Top 7 GTA Industrial Submarkets for Leasing

Top 7 GTA Industrial Submarkets for Leasing

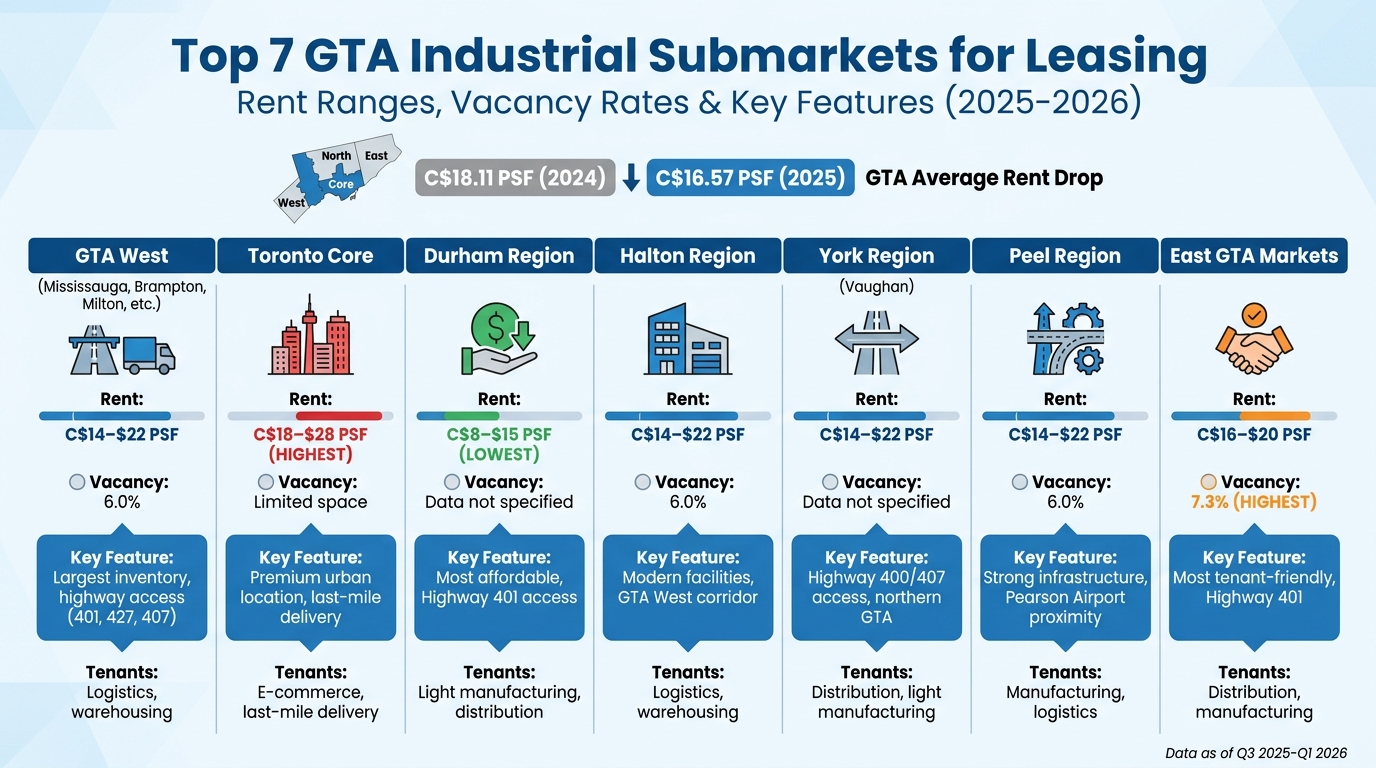

The Greater Toronto Area (GTA) industrial market is shifting, offering tenants more options and negotiating power. After years of rising rents, average asking lease rates fell from $18.11 per square foot in 2024 to $16.57 by the end of 2025, with vacancy rates climbing across the region. Here's a breakdown of the top submarkets:

- GTA West (Mississauga, Brampton, Milton, etc.): Largest inventory, strong highway access, rents between $14–$22 PSF. Ideal for logistics and warehousing.

- Toronto Core: Limited space, premium rents ($18–$28 PSF), great for last-mile delivery and e-commerce.

- Durham Region: Most affordable ($8–$15 PSF), suited for cost-sensitive businesses like light manufacturing.

- Halton Region (Oakville, Burlington, etc.): Modern facilities, rents at $14–$22 PSF, attracting logistics and warehousing.

- York Region (Vaughan, etc.): Competitive rents ($14–$22 PSF), excellent for distribution due to Highway 400/407 access.

- Peel Region (Mississauga, Brampton): Strong infrastructure, rents at $14–$22 PSF, recovering from oversupply.

- East GTA Markets: Tenant-friendly with high vacancy (7.3%), rents at $16–$20 PSF, good for distribution and manufacturing.

Quick Comparison:

| Submarket | Rent Range (C$ PSF) | Features | Key Tenants |

|---|---|---|---|

| GTA West | $14–$22 | Largest hub, highway access | Logistics, warehousing |

| Toronto Core | $18–$28 | Urban proximity, limited space | E-commerce, last-mile delivery |

| Durham Region | $8–$15 | Budget-friendly, Highway 401 | Light manufacturing, distribution |

| Halton Region | $14–$22 | Modern facilities, prime location | Logistics, warehousing |

| York Region | $14–$22 | Highway 400/407 access | Distribution, light manufacturing |

| Peel Region | $14–$22 | Strong infrastructure | Manufacturing, logistics |

| East GTA Markets | $16–$20 | Tenant-friendly, Highway 401 | Distribution, manufacturing |

The GTA's industrial market is evolving. With rising vacancies and falling rents, now is a good time for businesses to secure flexible leases or upgrade to modern facilities.

GTA Industrial Submarkets Comparison: Rent Ranges and Key Features

The Clock is Ticking: Why Industrial Tenants Must Negotiate Leases Now

sbb-itb-1862e65

1. GTA West (Mississauga, Brampton, Milton, Halton Hills, Oakville, Burlington, Caledon)

The GTA West has become a powerhouse for industrial development, driven by a wave of large-bay warehouse approvals during 2021–2022. These new projects are now reshaping the industrial market as they come online, creating fresh opportunities and challenges.

Vacancy Rates

Vacancy rates in the GTA West have risen significantly, reaching 6.0% by early 2026, compared to just 1.1% in 2022. This increase is largely due to a surge in speculative large-format developments in outer markets, which has temporarily outpaced demand.

Average Asking Rent (C$ PSF)

Rental rates in the GTA West have seen a notable decline, mirroring broader market trends. By Q2 2025, the average asking net lease rate dropped to C$16.82 PSF, down from C$18.11 PSF the year before. This adjustment has given tenants more room to negotiate as landlords recalibrate their expectations. These shifts reinforce the area's appeal as a logistics hub, offering competitive costs for modern industrial space.

"Much of this increase continues to be driven by large-bay product in outer markets - namely the GTA West and East regions - where new developments approved in the aggressive 2021–2022 cycle are still coming online."

- Joe Rosati, Industrial Real Estate Broker

Proximity to Transportation and Logistics Hubs

The GTA West's location remains a major draw for businesses. With easy access to Pearson International Airport and Highway 401, the region continues to attract logistics operators, third-party logistics (3PL) providers, and manufacturers. This strategic positioning has fuelled demand for large-block leases, with deals exceeding 100,000 square feet making up nearly 50% of new leasing activity in 2025.

Key Tenant Types and Industry Presence

Thanks to its logistical strengths, the GTA West supports a wide range of industries. In 2025, nearly 49.6% of new leasing involved large-block spaces, while smaller spaces under 50,000 square feet accounted for 81.1% of transactions. The region's modern warehouses and transportation advantages make it a preferred choice for logistics operators, 3PL providers, manufacturers, and e-commerce fulfilment centres. These diverse tenant types highlight the area's role as a cornerstone of industrial activity in the Greater Toronto Area.

2. Toronto Core

The Toronto Core - including areas like Etobicoke, the Junction Triangle, Scarborough, and East York - faces a unique challenge: a severe shortage of land available for industrial development. Within Toronto proper, finding new industrial space is increasingly difficult, as the supply of developable land has nearly dried up. Meanwhile, demand for urban industrial facilities continues to climb. This tight market environment has led to higher rental rates and emphasizes the importance of urban connectivity.

Average Asking Rent (C$ PSF)

Industrial spaces in premium urban areas like Etobicoke and the Junction Triangle command net lease rates ranging from C$18 to C$28 per square foot (PSF). These rates significantly exceed the Greater Toronto Area (GTA) average of C$16.82 PSF, recorded in Q2 2025. On top of that, tenants face additional costs - such as taxes, insurance, and maintenance - adding C$3 to C$8 PSF annually. These elevated prices reflect the strategic importance of the Toronto Core, where proximity to densely populated urban areas reduces freight distances and cuts transportation costs.

"Developable industrial land in Toronto proper has become scarce, constraining new supply while demand continues growing. This supply-demand imbalance supports rental rate appreciation."

- Allen Mayer

Proximity to Transportation and Logistics Hubs

The Toronto Core stands out for its excellent connectivity, which is vital for efficient distribution networks. Western areas like Etobicoke enjoy easy access to the Gardiner Expressway, Highway 427, and are close to Pearson International Airport. Similarly, Scarborough and East York benefit from direct links to Highway 401 and the Don Valley Parkway (DVP). This extensive multimodal infrastructure - covering highways, rail terminals, and port facilities - supports both regional and international logistics.

Key Tenant Types and Industry Presence

The limited availability of space, combined with urban accessibility, has shaped the tenant landscape in the Toronto Core. Businesses prioritizing last-mile delivery and quick order fulfilment are especially drawn to this area. The tenant mix includes e-commerce companies, third-party logistics providers, food and beverage distributors, and light manufacturers. Additionally, there’s a rising need for cold chain facilities to handle fresh food delivery. Retailers are also seeking spaces that can manage both online order fulfilment and restocking for physical stores. The area’s public transit access further supports operations that rely heavily on labour.

3. Durham Region

Durham Region, which includes Pickering and Ajax, has become a budget-friendly choice for businesses looking to cut costs while maintaining access to essential transportation routes. Industrial lease rates in the area range from C$8 to C$15 PSF net, with additional operating costs between C$3 and C$8 PSF. This makes it the most affordable industrial submarket in the Greater Toronto Area (GTA).

Average Asking Rent (C$ PSF)

Durham's industrial space costs about half as much as urban Toronto, where rates range from C$18 to C$28 PSF. Suburban areas like Mississauga, Brampton, and Vaughan offer rents between C$14 and C$22 PSF, still making Durham 45%–75% cheaper. This pricing appeals to businesses like distribution centres and light manufacturers that need cost-effective solutions while staying connected to major highways.

Proximity to Transportation and Logistics Hubs

One of Durham's strongest assets is its direct connection to Highway 401, a critical route for businesses serving eastern Ontario and neighbouring regions. While it doesn't have the urban proximity of downtown Toronto or the airport access offered by Mississauga, Durham's location is ideal for companies focused on eastern markets. Its efficient transportation links make it a smart choice for logistics and supply chain operations.

Key Tenant Types and Industry Presence

Durham Region is especially attractive to e-commerce fulfilment centres, third-party logistics (3PL) providers, and light manufacturing companies. These businesses value the region's lower costs and easy access to eastern transportation corridors. Another major advantage is Durham's ability to accommodate large distribution centres exceeding 200,000 square feet, a critical factor as land availability in the central GTA becomes increasingly limited. These strengths set the stage for a comparison with Halton Region in the following analysis.

4. Halton Region

Halton Region, part of the GTA West industrial submarket, is experiencing notable shifts in tenant strategies and market dynamics. Covering Oakville, Burlington, Milton, and Halton Hills, this area has seen significant changes in recent years. By Q4 2025, the vacancy rate reached 6.0%, a marked jump from just 1.1% in 2022. This rise is largely due to a surge of large-bay speculative developments that were greenlit during the active 2021–2022 period.

Vacancy Rates

Vacancy rates across Halton vary widely depending on property size. Large warehouses over 200,000 square feet face a vacancy rate of 6.7%, while mid-to-large properties between 100,000 and 200,000 square feet are much tighter at just 2.5%. Smaller properties under 20,000 square feet have a vacancy rate of 5.9%. Overall, Halton's vacancy rate of 6.0% remains lower than the GTA East submarket's 7.3%. This increase in vacancies has shifted the balance of power toward tenants, with landlords now offering more concessions and greater lease flexibility.

Average Asking Rent (C$ PSF)

Industrial rents in Halton have eased, following a broader trend across the GTA. Victor Cotic of Colliers reports that as of Q3 2025, GTA industrial rents averaged C$16.84 per square foot, reflecting a C$1.62 (4%) decrease from their Q3 2023 peak. While new construction is expected to slow significantly by late 2026, the current market environment is giving tenants an edge, with more favourable lease terms becoming common. This cooling in rents is reshaping the tenant landscape in Halton.

Key Tenant Types and Industry Presence

Leasing activity in Halton is primarily driven by small to mid-sized businesses occupying spaces under 50,000 square feet. However, there's a noticeable resurgence of large-block deals in 2025, following a quieter 2024. Logistics providers, 3PL companies, and manufacturers are returning to the market, drawn to Halton's prime position within the GTA West corridor.

"It feels, for the first time in several quarters, like the market is searching for a new equilibrium instead of being paralyzed by uncertainty." - Joe Rosati, Industrial Real Estate Broker

This uptick in activity reflects a cautious but growing confidence among decision-makers, who are beginning to make selective moves despite lingering economic challenges.

5. York Region

York Region, centred around Vaughan's industrial hub, is strategically positioned at the intersection of Highway 400 and Highway 407. This prime location offers excellent logistics advantages, making it a key distribution point for businesses serving the northern GTA and beyond. The area is well-regarded for its Class A facilities, which attract tenants focused on efficiency and connectivity. These factors contribute to competitive lease rates and a diverse mix of tenants.

Average Asking Rent (C$ PSF)

Lease rates in York Region typically fall between C$14 and C$22 per square foot net. On top of that, operating costs range from C$3 to C$8 PSF annually. As Allen Mayer puts it, "Vaughan industrial real estate offers modern facilities and competitive lease rates". This makes the region an appealing choice for businesses looking for high-quality spaces without the premium costs of downtown locations.

Proximity to Transportation and Logistics Hubs

The Highway 400/407 interchange is a major factor in York Region's industrial success. It provides seamless access to northern Ontario markets while connecting efficiently to the rest of the GTA through the 407 ETR toll route. This strategic location allows businesses to streamline their supply chain operations, improving delivery times and cutting transportation expenses. Such connectivity is a critical asset for companies operating in the region.

Key Tenant Types and Industry Presence

York Region is home to a range of tenants, including e-commerce fulfilment centres, third-party logistics (3PL) providers, and light manufacturing firms. These businesses are particularly drawn to warehouses offering clear heights of over 30 feet and infrastructure designed for fast distribution. Additionally, the growing trend of "safety stock" inventory strategies - shifting away from just-in-time models - has fuelled ongoing demand for expansive warehouse spaces in the area.

6. Peel Region

Peel Region, which includes Mississauga and Brampton, plays a key role in the GTA West industrial market. With the market cooling and tenants gaining more leverage, the area has experienced a wave of large-bay warehouse completions since 2022. This shift has opened doors for tenants seeking state-of-the-art facilities and better negotiating power.

Vacancy Rates

As of early 2026, Peel Region's vacancy rate climbed to 6.0%, a notable increase from just 1.1% in 2022. This change is linked to the addition of 26.5 million square feet of industrial space since late 2022, representing 16.2% of the submarket’s total inventory. These new large-bay developments have reshaped the market landscape. While vacancy rates have eased from their record lows, Peel’s rate remains below the 7.3% seen in GTA East. Additionally, over 6.2 to 7 million square feet of sublease space is available across the GTA, further tipping the scale in favour of tenants. This environment is fostering more competitive lease agreements.

Average Asking Rent (C$ PSF)

Lease rates in Peel Region have softened, with the average asking rent sitting at approximately C$16.57 PSF net as of early 2026, aligning with the GTA average. This decline reflects a market that is giving tenants more room to negotiate favourable terms. Despite the drop in rents, Peel’s robust infrastructure continues to attract businesses.

Proximity to Transportation and Logistics Hubs

Peel Region’s strategic location near Pearson International Airport and major 400-series highways (401, 407, 410) provides exceptional connectivity for logistics operators, distribution centres, and manufacturers. This access helps businesses cut delivery times and manage transportation costs, which is crucial in today’s competitive supply chain landscape.

Key Tenant Types and Industry Presence

In 2025, small- to mid-sized tenants (occupying less than 50,000 square feet) were responsible for 81.1% of all leasing activity. Meanwhile, large-block leases (100,000+ square feet) accounted for nearly half of all new deals during the same period. This trend signals a comeback for large tenants, drawn by Peel’s modern facilities and prime location. Goran Brelih, Executive Vice President at Cushman & Wakefield, elaborates:

"Large-block absorption is the key to working through the current oversupply of big-box warehouses, and the 2025 data suggests that large tenants - whether logistics operators, 3PLs, or manufacturers - are re-entering the market".

This renewed interest from larger tenants underscores confidence in Peel’s industrial market. Businesses and stakeholders looking to navigate these changing conditions can benefit from tailored leasing strategies and expert advice from Michael Law at Lennard Commercial – Industrial Real Estate Services (https://mlawrealestate.com).

7. East GTA Markets

The East GTA has seen the sharpest change among all submarkets in the region. Vacancy rates jumped from a mere 0.3% in 2022 to 7.3% by early 2026 - a staggering 7.0 percentage point rise. This shift reflects both the influx of new industrial space and lower preleasing activity for these developments. With vacancy rates even higher than the 6.0% reported in the GTA West submarket, the East GTA has become a tenant-friendly environment. These changing conditions highlight unique rental trends and tenant behaviours in the area.

Vacancy Rates

Between late 2022 and 2025, the East GTA added 9.2 million square feet of industrial space, accounting for 6.6% of the region's total inventory. During the growth period of 2020–2022, preleasing rates for new developments typically ranged between 60% and 80%. However, by 2025, that average had plummeted to just 29.1%. Goran Brelih, Executive Vice President at Cushman & Wakefield, commented:

"GTA East stands out as the most dramatic case - from a vacancy rate of just 0.3% in 2022 to 7.3% today, a 7.0 percentage point swing that reflects both the scale of new supply delivered and the lower preleasing rates on that product."

This drop in preleasing rates has reinforced the tenant-friendly landscape. As vacancies rise, landlords are increasingly offering rental concessions to attract tenants.

Average Asking Rent (C$ PSF)

Rental prices in the East GTA have eased, with rates falling to C$16.82 per square foot by mid-2025. Landlords are adjusting rents to address the extended time properties are spending on the market. This trend signals a broader market recalibration.

Proximity to Transportation and Logistics Hubs

The East GTA, including areas such as Oshawa, boasts prime access to Highway 401, allowing logistics operators to reach nearly 50% of Canada's population within a single day's drive. While more affordable than premium submarkets, the East GTA offers excellent transportation connectivity via Highway 401, making it an appealing location for distribution centres, light manufacturing, and value-add redevelopment opportunities.

Key Tenant Types and Industry Presence

The East GTA reflects broader market trends, with most activity involving small- to mid-sized transactions. However, there has been a noticeable rebound in large-block leasing. This resurgence indicates growing confidence among logistics operators, third-party logistics providers, and manufacturers, who are taking advantage of better negotiating terms and state-of-the-art facilities. Businesses navigating this evolving market can benefit from expert advice - Michael Law at Lennard Commercial – Industrial Real Estate Services (https://mlawrealestate.com) offers tailored leasing strategies backed by extensive market expertise.

Submarket Comparison Table

Here's a quick look at the top seven GTA industrial submarkets, highlighting average asking rents, key features, and typical tenant profiles.

| Submarket | Avg. Asking Rent (C$ PSF) | Main Characteristics | Primary Tenant Types |

|---|---|---|---|

| GTA West (Mississauga, Brampton, Milton, Halton Hills, Oakville, Burlington, Caledon) | C$14.00–C$22.00 | Largest industrial hub with excellent highway access (401, 427, 407) and a vast inventory | Logistics, distribution, large-scale warehousing |

| Toronto Core | C$18.00–C$28.00 | Limited land availability, higher rents, and close proximity to dense urban areas, ideal for last-mile delivery | E-commerce fulfilment, urban logistics, last-mile delivery |

| Durham Region | C$8.00–C$15.00 | Cost-effective market with competitive lease rates and access to eastern Ontario | Regional distribution, light manufacturing, value-add operations |

| Halton Region | C$14.00–C$22.00 | Part of the GTA West corridor with strong highway connectivity and modern facilities | Logistics, warehousing, distribution |

| York Region | C$14.00–C$22.00 | Northern GTA access with modern business parks and Highway 400/407 connections | Flex industrial, tech manufacturing, logistics |

| Peel Region | C$14.00–C$22.00 | Key part of GTA West with significant inventory, typically more affordable than Toronto Core | Manufacturing, warehousing, distribution |

| East GTA Markets | C$16.00–C$20.00 | Tenant-friendly environment with easy access to Highway 401 | Third-party logistics, distribution centres, light manufacturing |

The GTA industrial market continues to evolve. By Q3 2025, the vacancy rate hit 4.2%, while sublease availability surpassed 7 million square feet. These figures highlight the absorption of new supply and a noticeable trend of tenants scaling back on surplus space.

Conclusion

GTA industrial submarkets cater to a wide range of tenant requirements. The Toronto Core stands out with premium rental rates ranging from C$18.00 to C$28.00 per square foot, paired with excellent access for last-mile delivery operations. Meanwhile, GTA West boasts the largest inventory in the region, supported by strong highway connectivity, making it a top choice for large-scale logistics and distribution. On the other hand, Durham Region offers more affordable pricing, between C$8.00 and C$15.00 per square foot, making it a practical option for businesses prioritizing cost savings over proximity to urban hubs. These unique characteristics highlight the diverse opportunities available in the current tenant-friendly market.

With a vacancy rate of 4.2% in Q3 2025 and over seven million square feet of sublease space now available, tenants are in a stronger position than they have been in years. This increase in sublease availability provides businesses with access to move-in-ready facilities that often come with flexible terms and more competitive rates compared to direct leases.

Key factors like building specifications and sublease opportunities are becoming essential for ensuring long-term operational success. Choosing the right submarket depends heavily on aligning location with specific business needs. For instance, companies needing access to northern GTA areas benefit from Vaughan's proximity to the Highway 400/407 interchange, while those targeting eastern Ontario markets gain an edge with Durham Region's Highway 401 connectivity. Professionals like Michael Law of Lennard Commercial bring expertise in industrial real estate across Toronto and the GTA, offering tailored solutions for leasing, acquisitions, and dispositions based on deep market knowledge and exclusive data.

This evolving market landscape gives businesses a rare chance to optimize their operations, secure flexible lease terms, or move into higher-quality facilities that may have been out of reach during tighter market conditions.

FAQs

Should I choose a direct lease or a sublease in the GTA right now?

Deciding between a direct lease and a sublease in the Greater Toronto Area (GTA) comes down to your priorities and the current real estate climate. With vacancy rates climbing and over seven million square feet of sublease space on the market, subleases can often mean lower costs and more flexibility. On the flip side, direct leases tend to offer more control and stability. It’s all about what matters most to you - whether it’s cutting costs or securing a long-term arrangement - in this evolving market.

Which GTA submarket is best for last-mile delivery versus regional distribution?

Urban and infill submarkets near Toronto's densely populated areas, such as Vaughan and Milton, are excellent for last-mile delivery. Their close proximity to major transportation routes makes them an ideal choice for quick and efficient deliveries.

For regional distribution, suburban areas like Vaughan and Milton also stand out. These locations typically feature larger warehouses, lower land costs, and convenient highway access, making them well-suited for serving larger regions and handling bulk distribution needs.

What lease concessions can tenants realistically negotiate in 2026?

By 2026, tenants in the GTA's industrial market might find themselves in a stronger position to negotiate perks such as lower rent, rent-free periods, or better lease terms. This shift could be attributed to easing rental rates and a modest rise in vacancy levels, creating more opportunities for favourable agreements.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist