Top 5 Challenges in Selling Distressed Industrial Properties

Top 5 Challenges in Selling Distressed Industrial Properties

Selling distressed industrial properties in the Greater Toronto Area (GTA) is tough. These properties often come with financial, physical, and legal hurdles, making transactions complex and time-consuming. Here's a quick breakdown of the top challenges and how to address them:

- Physical Condition & Risks: Neglected maintenance, outdated infrastructure, and contamination issues scare off buyers. Conduct thorough inspections and provide clear remediation plans.

- Title Defects & Legal Barriers: Liens, unpaid taxes, and incomplete title chains complicate sales. Resolve these issues early with expert legal help.

- Tenant Issues: Unpaid rent, below-market leases, or unclear agreements lower property value. Audit leases, stabilize occupancy, and resolve disputes upfront.

- Market Positioning: Buyers often focus on flaws rather than potential. Use data-driven pricing and marketing to highlight investment opportunities.

- Financing & Timelines: High interest rates and long sales processes deter deals. Target private equity and streamline transactions with clear financial records.

Top 5 Challenges in Selling Distressed Industrial Properties (GTA)

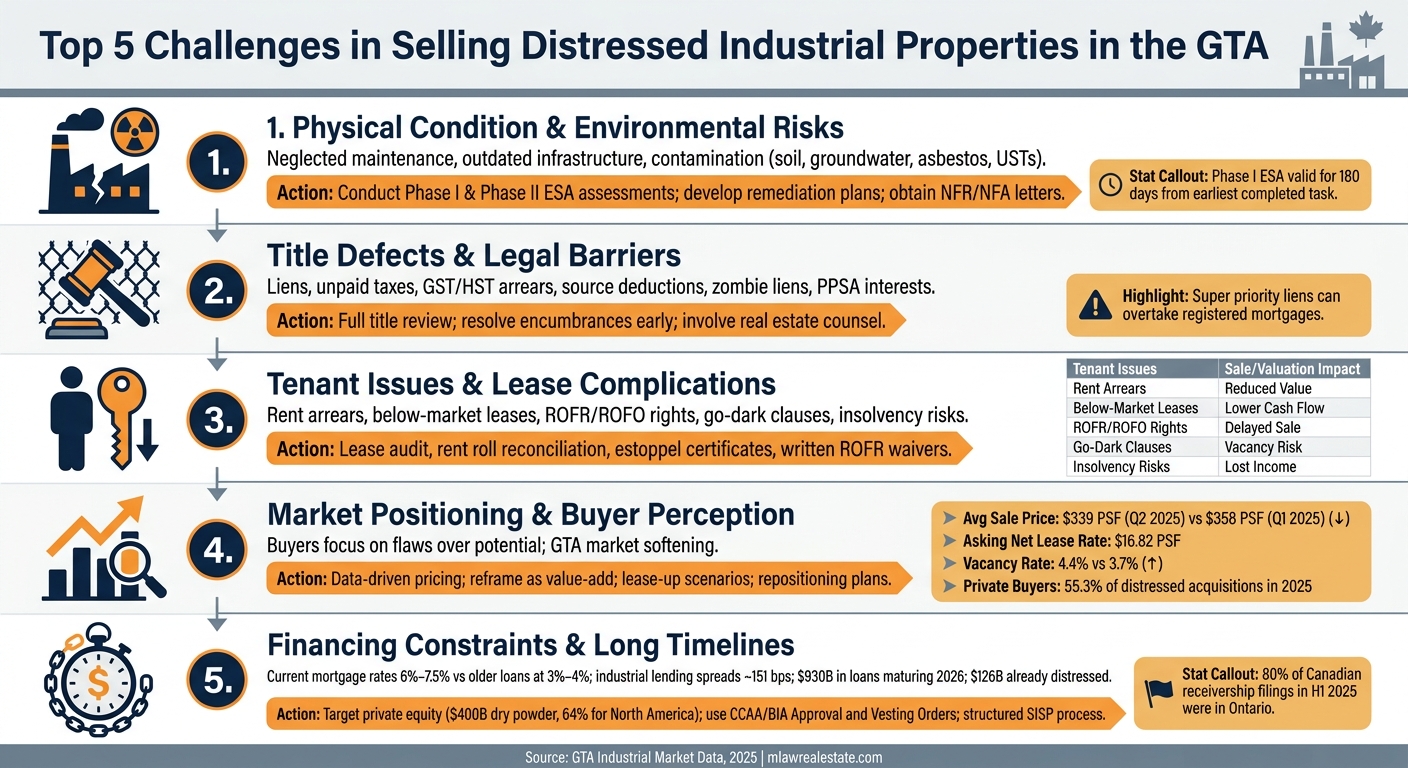

Challenge 1: Physical Condition and Environmental Risks

Physical wear and environmental liabilities are major hurdles for buyers of distressed industrial properties. These factors increase perceived risks, complicate financing, and can delay or even derail transactions. They also set the stage for other challenges related to title, tenancy, and financing.

Assessing Physical Condition and Maintenance Backlogs

Distressed industrial properties often show visible signs of neglect - roof damage, cracked foundations, rusted frames, and utilities that no longer function. Key areas like loading docks, equipment pads, and storage structures may be unsafe or unusable. Such problems directly affect property valuations and make lenders more cautious.

"An industrial building that was code-compliant under its previous use does not necessarily meet current requirements for a different operation." - Birchwood Law

Before listing a property, sellers should conduct a detailed condition assessment. This process helps identify deferred maintenance issues, estimate remediation costs, and avoid surprises during due diligence. Since retrofitting can be expensive, catching these issues early is critical. Once physical deficiencies are documented, the focus should shift to environmental risks.

Addressing Environmental Risks and Regulatory Compliance

Environmental concerns often complicate the sale of distressed industrial properties. Common risks include soil and groundwater contamination, leaking underground storage tanks, asbestos, lead-based paint, and chemical residues from past operations. Buyers may inherit responsibility for these issues under environmental law, making thorough due diligence a must.

The first step is typically a Phase I Environmental Site Assessment (ESA) following ASTM E1527-21 standards. This process identifies recognized environmental conditions (RECs). If RECs are found, a Phase II ESA - covering soil, groundwater, and material sampling - is required to assess the extent of contamination. Keep in mind that a Phase I ESA has a 180-day validity period from the earliest completed task, so if a deal is delayed, elements like interviews, lien searches, and site visits may need to be updated.

"The 180-day shelf life for a Phase I ESA runs from the earliest completed critical task, not the report date... If a deal timeline slips, interviews, lien searches, regulatory records, and the site visit often must be refreshed." - J. Michael Showalter and Joshua R. More, ArentFox Schiff LLP

Sellers should also stay informed about evolving regulations. For example, starting in July 2024, the EPA will classify PFOA and PFOS - chemicals linked to firefighting foam and certain industrial processes - as hazardous substances under CERCLA. Any release over one pound within 24 hours will require immediate reporting. Properties with a history of such operations may need PFAS screening as part of a Phase II ESA.

Presenting Findings to Build Buyer Confidence

Transparency is key to overcoming physical and environmental challenges. By sharing assessment reports, estimated remediation costs, and detailed remediation plans, sellers can demonstrate good faith and reduce buyer uncertainty. Practical steps include organizing documentation with site maps and photo records linked to RECs. Sellers might also consider participating in provincial brownfield or voluntary cleanup programs to secure a No Further Remediation (NFR) or No Further Action (NFA) letter. These documents provide buyers and lenders with added liability protection.

For properties with ongoing environmental obligations, clear operational guidelines can help buyers understand post-closing compliance requirements. When environmental risks are well-documented and tied to cost estimates, they become points for negotiation rather than deal-breakers. Tackling these concerns early is vital to presenting distressed assets as attractive investment opportunities.

sbb-itb-1862e65

Challenge 2: Title Defects, Liens, and Legal Barriers

Once physical and structural concerns are resolved, legal issues often emerge as the next hurdle. Distressed industrial properties tend to come with a host of financial and legal complications - like unpaid property taxes, construction liens, writs of execution, unregistered easements, or incomplete chains of title. These unresolved problems can delay sales, make financing difficult, and complicate insurable ownership. Clearing these hurdles is a necessary step before addressing tenant concerns and market positioning.

Identifying and Clearing Title Encumbrances

The process starts with a detailed title review - this goes beyond a simple parcel register search. You'll need to uncover potential issues such as writs, PPSA security interests, super priority liens, and even "zombie" liens (outstanding liens that were never formally released). Super priority liens are particularly concerning because they can take precedence over registered mortgages. These often include unpaid property taxes, GST/HST arrears, and source deductions. Zev Zlotnick, a Partner at Gardiner Roberts LLP, highlights the seriousness of these claims:

"Super priority liens most commonly include unpaid property tax, GST/HST, source deductions and in some instances, environmental liens... these liens will take, or overtake, priority over the mortgage security."

Another common issue arises when loans have been paid off but the lender fails to file a formal discharge, leaving outdated registrations on the title. Identifying and clearing these issues is crucial before moving forward with a sale.

Structuring Deals to Reduce Legal Risk

Once title encumbrances are addressed, the focus shifts to structuring the deal in a way that minimizes legal risks. Financial liens can often be discharged using proceeds from the sale, but construction liens are trickier - they require either a settlement or a court order for resolution. On this matter, Zlotnick advises:

"lenders cannot unilaterally discharge a lien through power of sale; a settlement or court order is required."

To navigate these complexities and ensure the deal progresses smoothly, it's critical to involve experienced real estate counsel early in the process. Their expertise can help you tackle these legal challenges head-on.

Challenge 3: Tenant Issues and Lease Complications

Once title and legal challenges are resolved, tenant-related problems often emerge as the next major obstacle in selling distressed industrial properties. These properties frequently come with messy tenancy situations - things like unpaid rent, below-market leases, informal agreements, or tenants with purchase rights that can delay or block a deal altogether. These complications can shake buyer confidence and slow down financing. Tackling tenant issues upfront is key to making the property as appealing and stable as possible.

Auditing and Organizing Lease Agreements

The starting point here is a thorough audit of all tenancy arrangements. This means gathering every lease document, verifying them, and creating a reconciled rent roll that matches actual bank statements and lease agreements. This step is crucial to identify any discrepancies. Alex Kolandjian, Partner at Fogler, Rubinoff LLP, emphasizes the importance of this process:

"The lease 'runs with the land', and purchasers may be exposed to ongoing or unforeseen liabilities or obligations if they do not conduct proper lease due diligence."

Another critical part of this audit is identifying tenant purchase rights, like Rights of First Refusal (ROFR) or Rights of First Offer (ROFO). These rights can interfere with a sale by giving tenants the chance to buy the property first, potentially delaying or even derailing your deal. To avoid this, secure written waivers for these rights as early as possible. Ignoring this step can have serious consequences, as seen in the Ontario case Sandhu v Paterson (2016 ONSC 1748), where the court upheld an existing lease because the buyer failed to properly investigate it.

Here’s a quick breakdown of common tenant issues and how they impact property valuation:

| Tenant Issue | Impact on Sale or Valuation |

|---|---|

| Rent Arrears | Reduces cash flow and complicates buyer financing |

| Below-Market Rent | Lowers Net Operating Income (NOI) and valuation |

| ROFR / ROFO | Can delay or block a sale to a third-party buyer |

| "Go Dark" Rights | Reduces marketability and risks co-tenancy defaults |

| Insolvency (BIA/CCAA) | May result in lease disclaimers, leading to sudden vacancies |

Resolving Tenant Conflicts and Stabilizing Occupancy

After auditing leases, the next step is resolving any conflicts or discrepancies to stabilize the property’s occupancy. For unpaid rent, Ontario landlords have a unique tool called distraint. This allows landlords to seize and sell a tenant’s personal property (like inventory or equipment) to recover unpaid rent - without needing a court order, provided the lease hasn’t been terminated. Typically, distraint can recover up to three months of arrears, plus three months of accelerated rent if the lease permits it. However, as Robins Appleby points out:

"The remedy of distraint and termination are like oil and water – they don't mix and the exercise of one, precludes the exercise of the other."

For informal or unclear agreements, an estoppel certificate can be a game-changer. This document confirms key tenancy details, such as rent, lease expiry, and any outstanding issues, locking in these facts so tenants can’t dispute them later. For leases nearing expiry, negotiating extensions is also smart. As noted in one case, "a purchaser will also not want to risk losing customer base as a result of having to relocate if the Landlord does not agree to grant further options to extend."

Challenge 4: Market Positioning and Buyer Risk Perception

Even after dealing with tenant-related hurdles, sellers of distressed industrial properties often face another significant challenge: overcoming buyer hesitations. These properties frequently carry a negative reputation, with buyers focusing more on current flaws than on potential future benefits. Bridging this perception gap requires a well-executed, data-informed marketing approach that clearly outlines the investment potential.

Building a Data-Driven Marketing Strategy

The industrial real estate market in the Greater Toronto Area (GTA) has seen some notable changes recently. Data reveals that average sale prices dropped to $339 per square foot (PSF) in Q2 2025, down from $358 PSF in Q1 2025. Similarly, average asking net lease rates declined to $16.82 PSF, marking the fourth consecutive quarter of decreases, while vacancy rates rose to 4.4% from 3.7%. Using these metrics strategically can help position distressed properties more competitively.

Aligning the pricing of a distressed property with these GTA averages can reassure buyers that the price reflects current market conditions rather than outdated valuations. Coupling this with a robust package that includes comparable sales data, local rent trends, and a detailed lease-up scenario provides buyers with the analytical tools they need to make informed decisions.

"Success will depend on detailed analysis coupled with a flexible strategy amid the uncertainty." - Forvis Mazars

The current GTA market is largely driven by occupier-buyers - businesses with specific operational needs and long-term goals - rather than speculative investors. However, value-add investors remain active, with private buyers making up 55.3% of all distressed acquisitions in 2025. Understanding these dynamics is key to crafting a targeted marketing strategy.

Shifting the Narrative from Distressed to Value-Add

The term "distressed" often implies risk, so it’s essential to reframe the property as a value-add opportunity. This doesn’t mean ignoring its challenges but rather highlighting its potential. As one expert puts it:

"When marketing distressed assets, it's not about the current condition - it's about the future potential. Illustrate the property's post-turnaround potential." - RealNex

This involves presenting clear, alternative business cases that outline a credible recovery plan. For example, a lease-up scenario with stabilised net operating income based on market rents, a repositioning plan for adaptive reuse, or a phased capital improvement strategy can help buyers envision a clear path to value. Justin Cox of The Vertex Companies emphasizes this point:

"Repositioning your existing real estate assets can achieve higher rates of return than ground-up real estate development." - Justin Cox, The Vertex Companies

Providing a transparent breakdown of capital requirements, timelines, and potential returns - grounded in GTA market benchmarks - can ease buyer concerns. Michael Law of Lennard Commercial specializes in creating this kind of positioning. By leveraging proprietary GTA market data, he helps sellers transform distressed properties into well-targeted investment opportunities that appeal to the right buyers.

Challenge 5: Financing Constraints and Long Transaction Timelines

Even after resolving issues like physical condition, legal complications, and tenancy problems, sellers of distressed industrial properties face two more significant hurdles: securing financing and managing lengthy transaction timelines. Financing these properties is especially tricky given the current commercial mortgage rates of 6%–7.5%, which are much higher than the 3%–4% rates on older loans. This increase in rates amplifies buyer risk. Adding to the difficulty, industrial properties come with lending spreads of approximately 151 basis points. Properties with declining occupancy or inconsistent cash flow often fail to meet debt service coverage ratios, leaving buyers unable to secure loans, no matter the property's potential.

Making the Property Easier to Finance

To attract financing, sellers need to minimize the risks faced by lenders. This starts with presenting clear and organized financial records, resolving title issues, and ensuring stable tenancy. As mentioned earlier, securing long-term leases before listing the property can significantly improve its appeal to lenders.

Another effective approach is targeting private equity and distressed-debt funds. These funds currently hold around $400 billion in dry powder, with 64% allocated for North America. Their willingness to take on higher risks can fill the gap when traditional banks hesitate. Additionally, offering flexible deal structures can provide further options for buyers struggling with conventional financing.

Once financing challenges are addressed, sellers must focus on managing the inherently long sales timeline.

Managing the Sales Timeline Effectively

The commercial real estate market is facing a looming challenge, with nearly $930 billion in loans set to mature in 2026, including $126 billion already classified as distressed.

"The wall of maturities is simply an indicator to watch. Prevailing interest rates and property pricing at the time of maturity will play an important role in how many of the upcoming loans will be refinanced." - Forvis Mazars

Starting the sales process early is crucial. In Ontario, for example, 80% of Canadian receivership filings in the first half of 2025 occurred within the province. Formal insolvency proceedings under the Companies' Creditors Arrangement Act (CCAA) or the Bankruptcy and Insolvency Act (BIA) can help streamline sales. Court-approved Approval and Vesting Orders discharge pre-existing liens, enabling buyers to acquire properties free and clear. Additionally, a well-structured Sales and Investor Solicitation Process (SISP), often supported by a stalking horse bidder, can give lenders the market validation they need to proceed with confidence.

"Ongoing challenges reflect the need for both lenders and insolvency practitioners to demonstrate patience and creativity in developing unique realization strategies for these properties in order to maximize value." - Jeffrey Oliver, Partner at Cassels, Brock & Blackwell LLP

The most successful sellers are those who prepare early, target the right sources of capital, and structure their deals to simplify financing. By doing so, they not only overcome these challenges but also turn them into opportunities. For sellers in Ontario, particularly in Toronto and the Greater Toronto Area, expert advice from Michael Law of Lennard Commercial - Industrial Real Estate Services can help navigate these complex processes and achieve smoother outcomes.

Conclusion: How to Successfully Sell Distressed Industrial Properties

Selling distressed industrial properties in the GTA can be tricky, but it’s far from impossible with the right approach. Start by tackling the property's physical condition and any environmental risks through detailed assessments and open, transparent reporting. Address title defects and legal hurdles early on by resolving encumbrances and, if needed, obtaining approval and vesting orders under the CCAA or BIA to ensure a clean title. Tenant-related issues, such as lease audits and stabilizing occupancy, should also be resolved before the property hits the market.

Once these foundational issues are managed, the focus shifts to repositioning the property for the market and planning the financial aspects. Highlight the property’s potential as a "value-add" investment using accurate data and realistic pricing to ease buyer concerns. To address financing and timeline challenges, ensure financial records are well-organized, tenancy is stable, and the solicitation process is structured to streamline financing and close deals faster.

As Gowling WLG aptly puts it, "There is no 'one-size-fits-all' acquisition structure in distressed M&A. Because each transaction is unique, prospective buyers of distressed assets need to look creatively at each transaction." Each distressed property brings its own mix of legal, physical, and market challenges, making a tailored strategy essential.

"A fair, transparent and well-documented sale process is [a lender's] best protection, particularly in challenging and rapidly changing market conditions." - Wildeboer Dellelce LLP

FAQs

What should I do first before listing a distressed industrial property in the GTA?

Before putting a distressed industrial property in the GTA on the market, it's crucial to do your homework. Start by thoroughly evaluating the property's condition. Check that it complies with zoning laws and environmental regulations, and make sure all legal and regulatory requirements are met. This process helps identify any potential risks and ensures the property aligns with your intended purpose.

How do Phase I and Phase II ESAs affect the sale price and closing timeline?

Phase I Environmental Site Assessments (ESAs) are used to pinpoint possible environmental risks that could influence property value. These risks often lead to adjustments in the purchase price. If concerns are flagged during Phase I, a Phase II ESA may be required. This phase involves in-depth testing, which can reveal expensive problems, potentially delaying the closing process and driving up costs. Together, these assessments can have a major effect on both the sale price and the timeline of the transaction.

Can tenant rights like ROFR/ROFO stop or delay my sale, and how do I deal with them?

Tenant rights, like Right of First Refusal (ROFR) or Right of First Offer (ROFO), can introduce delays or complexities into a sale if the tenant decides to exercise these rights. That said, they don’t outright block the transaction from happening. The key to managing these situations lies in conducting thorough due diligence and negotiating terms clearly. This approach helps address these rights effectively, paving the way for a smoother sale process.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist