GTA Industrial Property Investment: 2026 Market Analysis

GTA Industrial Property Investment: 2026 Market Analysis

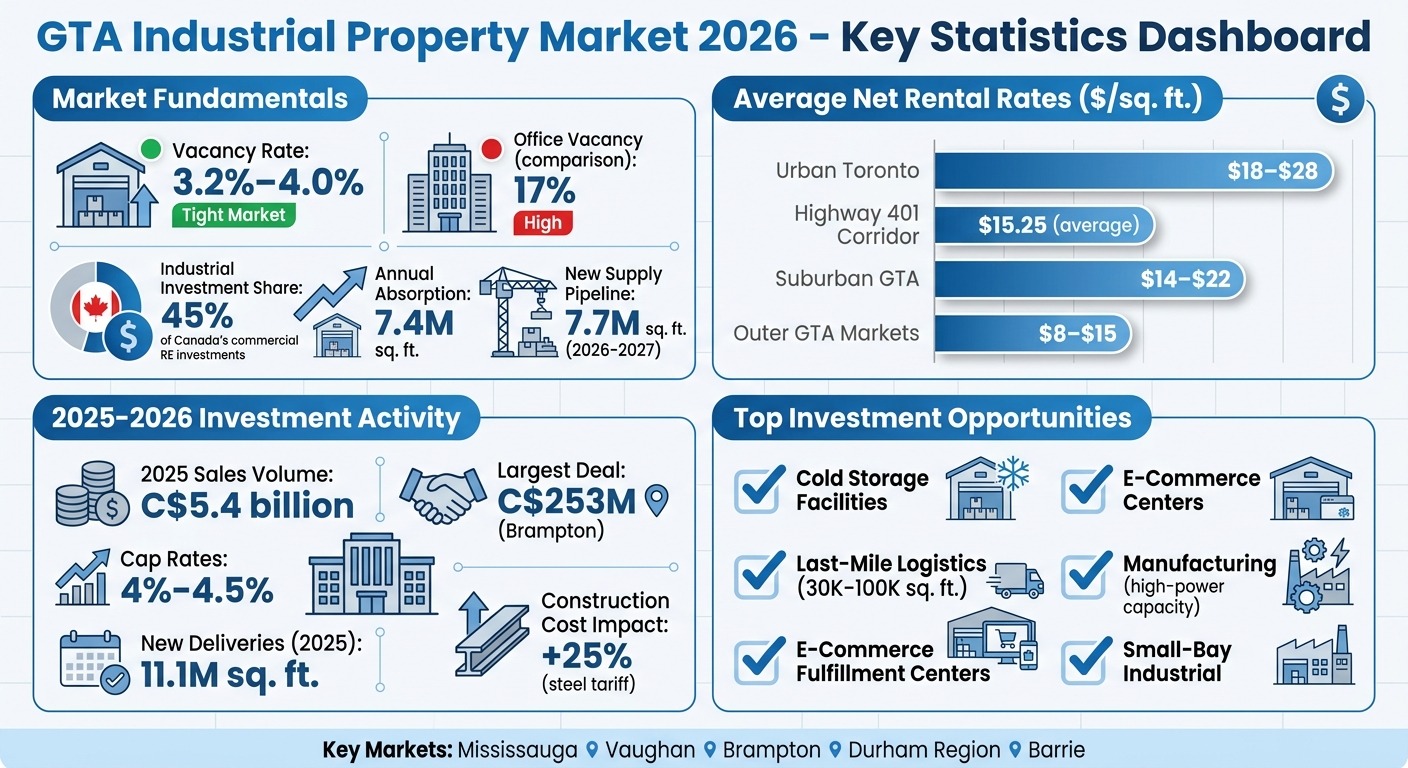

The GTA industrial real estate market in 2026 is defined by low vacancy rates (3.2%–4%), rising rents, and strong investor demand. Key highlights include:

- Rental Rates: Highway 401 corridor warehouses average $15.25/sq. ft., while urban Toronto spaces reach $18–$28/sq. ft.

- Vacancy Trends: Industrial vacancies remain tight, unlike downtown office spaces with 17% vacancy.

- Investor Focus: Industrial properties now represent 45% of Canada’s commercial real estate investments.

- Emerging Trends: High-power electrical capacity is critical due to demand from data centres and AI projects.

- Key Property Types: Cold storage, last-mile logistics, and manufacturing facilities are in high demand.

With limited new supply (7.7M sq. ft. under construction for 2026–2027) and rising construction costs, the GTA remains a landlord’s market. Investors are targeting areas like Mississauga, Vaughan, and Brampton for their logistics advantages, while outer regions like Durham and Barrie offer cost-effective opportunities.

Takeaway: The GTA industrial market is poised for continued growth, driven by e-commerce, reshoring, and supply chain shifts. For investors, focusing on well-located, modern facilities with specialized features is key to maximizing returns.

GTA Industrial Real Estate Market 2026: Key Statistics and Regional Comparison

Q2 Market Update: Industrial Real Estate at a Turning Point

sbb-itb-1862e65

GTA Industrial Market Overview in 2026

The industrial real estate market in the Greater Toronto Area (GTA) remains exceptionally tight in 2026, with vacancy rates hovering between 3.2% and 4.0%. This reflects strong tenant demand and stands in stark contrast to the downtown Toronto office market, where vacancies are significantly higher at around 17%. The scarcity of industrial space has created a competitive landscape, giving landlords the upper hand while limiting tenant options.

"What we're seeing is a market so tight that finding available industrial space has become genuinely difficult, and that scarcity is creating both opportunities and challenges for anyone involved in this sector." – Ehsan, Innovative Property Solutions

Vacancy Rates, Rental Prices, and Absorption

The high demand for industrial space is evident in rental prices. Along the Highway 401 corridor, modern warehouse facilities command an average net lease rate of $15.25 per square foot. However, rental rates vary widely depending on location:

- Urban Toronto (e.g., Etobicoke, Junction Triangle): $18 to $28 per square foot net

- Suburban GTA (e.g., Mississauga, Brampton, Vaughan): $14 to $22 per square foot net

- Outer GTA markets (e.g., Durham Region, Barrie): $8 to $15 per square foot net

Demand remains strong, with annual absorption reaching 7.4 million square feet in 2026, including 5.8 million square feet absorbed in the GTA during late 2025. Smaller industrial spaces catering to last-mile delivery operations are particularly sought after, even as larger manufacturing tenants proceed cautiously due to ongoing trade discussions with the United States. This demand paints a clear picture of the pressures facing the region's supply chain.

Supply Challenges and New Construction

In 2025, the GTA saw 11.1 million square feet of new industrial space delivered. However, only 7.7 million square feet are under construction for 2026–2027, highlighting a constrained development pipeline. Several factors are contributing to this slowdown:

- Rising construction costs: A 25% tariff on imported steel has significantly increased expenses for developers.

- Insufficient rental growth: Current rent levels fall short of what’s needed to justify new builds.

"The rent levels required to make new industrial construction financially viable remain well above what the current market will support." – Tanis Read, Managing Broker, Coldwell Banker Horizon Realty

Adding to the challenge is the scarcity of developable land, particularly near key highway interchanges and urban centres. With much of the GTA already built out, the value of existing industrial properties - especially modern facilities in prime logistics locations - continues to rise. For investors, this limited supply and rising demand reinforce the appeal of holding or acquiring well-located industrial assets.

Investment Trends and Forecasts for 2026

What's Driving Demand: E-Commerce, Cold Storage, and Manufacturing

In 2026, three major forces are reshaping the industrial real estate market in Canada: the continued rise of e-commerce, the growing need for cold storage, and a resurgence in manufacturing. These trends are driving demand for warehouse space, making the industrial sector a dominant player - accounting for roughly 45% of total commercial real estate investment in the country.

Supply chain strategies have shifted significantly, moving away from "just-in-time" models to "just-in-case" approaches. This change prioritizes resilience, with businesses holding more inventory closer to customers. As a result, regional warehouse spaces are becoming increasingly vital.

"The combination of e-commerce growth, supply chain repositioning, and reshoring creates demand from multiple directions simultaneously - making GTA industrial real estate one of the most fundamentally sound investment categories in Canada's commercial property market." – Seven Appraisal Inc.

Manufacturing is also seeing a revival, fuelled by nearshoring efforts that focus on North American production to mitigate supply chain risks. Additionally, cold storage facilities are emerging as a critical investment area. With rising demand for fresh food and pharmaceutical delivery, these temperature-controlled spaces are in high demand. They often command premium rents despite requiring significant capital investment, offering consistent, long-term returns as the cold chain infrastructure expands.

Another key trend is the increasing importance of high-capacity electrical connections. As AI infrastructure and data centres compete with traditional logistics for "power-ready" sites, these connections have become more valuable than square footage in some cases.

These shifts in demand are creating unique opportunities across the Greater Toronto Area (GTA), with each submarket offering distinct advantages.

Regional Performance and Where to Invest

The GTA's industrial market is thriving, with specific regions standing out for their unique strengths. The Highway 401 corridor, stretching from Burlington to Markham, remains a prime location. As one of North America's busiest freight corridors and home to over half of Canada's population within a day's drive, this area is a key logistics hub.

Mississauga leads as the GTA's largest industrial market, boasting extensive inventory and excellent highway connectivity, making it a top choice for logistics and distribution. Vaughan, located at the Highway 400/407 interchange, commands premium rents due to its strategic access to northern GTA regions. Meanwhile, Brampton offers more affordable options, making it ideal for large-scale manufacturing and distribution operations.

Toronto West, including areas like Etobicoke and the Junction Triangle, has the highest pricing in the region, with net rents ranging from $18 to $28 per square foot. Its proximity to the urban core and access to major routes like the Gardiner Expressway and Highway 427 make it a hub for last-mile delivery operations, serving over 6 million GTA residents.

For investors looking for value, outer GTA markets like Durham Region and Barrie are gaining traction. With rents between $8 and $15 per square foot net, these areas offer cost-effective alternatives as land scarcity in central markets intensifies. As the GTA continues to expand outward, these regions are well-positioned for growth.

The small-bay industrial segment also stands out, as it caters to local businesses that are less affected by global trade fluctuations. Additionally, favourable monetary conditions are expected to support consumer spending, driving demand in transportation, distribution, and warehousing sectors. However, trade policy remains an unpredictable factor, particularly in Toronto East, where steel and automotive manufacturing are concentrated. Resolving U.S.-Canada trade disputes could unlock significant demand for manufacturing space.

Industrial Property Types with Growth Potential

Cold Storage and Food-Grade Facilities

Cold storage facilities are emerging as prime investment opportunities in the Greater Toronto Area (GTA) for 2026. The rise of online grocery shopping and direct-to-consumer food delivery has created a growing need for refrigerated warehouse infrastructure. These facilities require significant upfront investment for advanced features like high-capacity refrigeration systems, ESFR sprinklers, and floors capable of supporting heavy loads (125–150+ lbs per square foot).

"Cold storage and specialized facilities serve food distribution, pharmaceuticals, and other products requiring temperature control. These buildings require significant capital investment in refrigeration systems but generate premium rents that justify the additional costs." – Innovative Property Solutions

While standard warehouse rents along the Highway 401 corridor average around $15.25 per square foot net, cold storage facilities command higher rates due to their specialized nature. The pharmaceutical industry's strict temperature needs, combined with rising consumer demand for fresh and prepared foods, ensure steady tenant interest. Proximity to key transportation hubs, such as the 401/400 interchange, is crucial for efficient last-mile delivery, enabling access to nearly half of Canada's population within a day's drive. Additionally, the growth of e-commerce continues to emphasize the need for strategically located facilities with robust power infrastructure.

E-Commerce and Last-Mile Logistics

The surge in online retail has amplified demand for properties tailored to modern logistics needs. High electrical capacity is now a key consideration for investors, as e-commerce fulfilment requires three times more warehouse space than traditional retail to handle equivalent sales volumes. Last-mile logistics facilities, typically sized between 30,000 and 100,000 square feet, thrive in urban areas near dense residential populations to meet same-day or next-day delivery expectations.

Urban hubs like Etobicoke and Junction Triangle see net rents ranging from $18 to $28 per square foot, driven by their strategic locations. Beyond location, access to high-capacity electrical power has become a critical factor in property value. As automation becomes central to last-mile efficiency, these facilities now compete with data centres for grid access, making electrical capacity as vital as square footage.

Manufacturing and Hazardous Material Storage

The reshoring of manufacturing to the GTA is fuelling demand for facilities with enhanced specifications. Modern manufacturing spaces need clear heights of 28–30 feet and floor-loading capacities exceeding 200 lbs per square foot - far above the requirements for standard warehouses. Submarkets like Toronto East, with its concentration of steel and automotive manufacturing, remain particularly sensitive to U.S.-Canada trade dynamics.

Facilities with high-capacity power connections are in high demand, often trading at a premium. Similarly, hazardous material storage facilities command higher rents due to their specialized safety features, such as ESFR sprinklers and compliance with strict regulations. This reshoring trend not only increases demand for manufacturing properties but also highlights the importance of facilities equipped to handle hazardous materials. For investors, ensuring properties meet electrical and structural specifications upfront is crucial, as retrofitting can be prohibitively expensive.

Investment Sales and Transaction Analysis

2025 Sales Volume and Major Deals

In 2025, the Greater Toronto Area (GTA) industrial market saw an impressive C$5.4 billion in sales volume, showcasing the growing importance of this asset class. One standout transaction was a C$253 million deal in Brampton, reflecting the aggressive pricing institutional investors are willing to pay for high-quality properties. Institutional players like pension funds, REITs, and insurance companies dominated the market, often outbidding private investors for larger facilities. This competitive bidding helped establish a pricing floor, providing stability to property values even amid broader economic challenges.

Cap rates for prime industrial properties tightened significantly, dropping to 4%–4.5%, compared to around 6% in previous years. Investors have been willing to accept lower returns, betting on future rent growth and property value appreciation. The scarcity of available properties has further solidified a landlord’s market, with tenants often committing to leases before construction is even completed. These strong 2025 figures have set the stage for an even more active market in 2026.

2026 Market Outlook and Deal Activity

Building on the momentum from 2025, transaction volumes are expected to grow in 2026 as borrowing costs stabilize and clearer trade policies encourage business expansion. After years of uncertainty, a more stable capital market is helping to restore confidence among both buyers and sellers.

However, new supply is anticipated to slow significantly. The GTA is nearing full development, and high construction costs continue to pose challenges for new projects. This limited supply, paired with the strength of the small-bay segment, will likely shape market dynamics in 2026. Small-bay properties, which cater to local businesses less exposed to global trade fluctuations, are expected to remain particularly strong.

With rental rates projected to keep climbing and institutional capital still heavily focused on industrial assets, the GTA industrial property market is poised for another competitive year. Supply constraints and sustained demand will likely drive further bidding wars, reinforcing the sector’s resilience and appeal.

Investment Strategies for GTA Industrial Properties

How to Acquire Properties and Negotiate Leases

With limited supply and fierce competition, securing high-quality industrial assets in the GTA requires a focused approach. Here are three effective investment models to consider:

- Core Income: Ideal for stabilized assets with reliable, creditworthy tenants.

- Value-Add: Focuses on upgrading older Class B or C properties to boost their value.

- Sale-Leaseback: Allows businesses to unlock capital while continuing operations on the property.

When scouting properties, prioritize those with direct access to major routes like Highway 401 or 400 - particularly in Vaughan. Locations near dense residential areas in Mississauga and Oakville are also strategic, especially for last-mile delivery operations. Additionally, ensure the property’s electrical systems can support specialized operations like manufacturing or cold storage.

Lease negotiations in 2026 require extra care. Expansion rights are critical - include ROFR (Right of First Refusal) or ROFO (Right of First Offer) clauses to secure future opportunities for adjoining spaces. With rents rising quickly, negotiate pre-set limits on renewal increases and secure the ability to audit and cap controllable operating costs. These costs typically add between C$3 and C$8 per square foot annually to the base rent.

Once acquisition strategies are in place, the next step is to fine-tune property sales and rent evaluations to maximize returns.

Selling Properties and Analyzing Market Rents

Recent transactions highlight the importance of precise valuations and rent strategies in achieving strong sale results. Start with a certified appraisal to ensure an accurate valuation in today’s competitive market. Properties with leases nearing expiration often attract buyers aiming to adjust rents to current 2026 market levels. In urban Toronto, net rents typically range from C$18 to C$28 per square foot, while suburban GTA areas command rates between C$14 and C$22 per square foot.

"An industrial building in Brampton or Vaughan could easily appraise for significantly more today than just a few years ago - based purely on rent growth and occupancy improvements, without any physical changes to the property."

- Seven Appraisal Inc.

Modern Class A facilities, with features like 30+ foot clear heights and ESFR sprinkler systems, tend to fetch higher premiums. These properties often achieve rental rates between C$16 and C$18 per square foot, compared to C$11 to C$13 for older, secondary assets.

Working with Lennard Commercial for Expert Guidance

Navigating the complexities of GTA industrial property investments can be challenging, but Lennard Commercial offers tailored expertise to help. Their services include:

- Lease renewal and relocation support, complete with detailed market rent analysis.

- Investment sale advisory, covering property valuation and connecting with the right buyers.

- Custom solutions for owner-occupied properties.

For specialized industrial spaces like cold storage, e-commerce fulfilment centres, hazardous material facilities, or high-power manufacturing sites, Lennard Commercial provides strategies backed by proprietary data and deep local knowledge. Their expertise spans across Toronto and the entire Greater Toronto Area, ensuring clients receive comprehensive support at every stage of their investment journey.

Conclusion: GTA Industrial Market in 2026

Main Points for Investors

The GTA industrial market is settling into a more stable phase. Vacancy rates are holding steady between 3.2% and 4%, reflecting tight market conditions that remain historically low. Meanwhile, average asking rents have adjusted to C$21.88 per square foot, a 4.9% decrease from the previous year, potentially opening doors for strategic investments.

Three major trends are shaping the market's trajectory. First, power capacity has emerged as a critical feature, with properties offering high-capacity electrical connections seeing increased demand. Second, institutional investors poured nearly C$15 billion into Canadian commercial real estate in 2025, signalling a resurgence of confidence in the market. Lastly, new supply is expected to remain limited through 2026 and 2027, as current rental rates are insufficient to offset rising construction costs, particularly with a 25% tariff on steel driving up expenses.

"What we're really watching is a normalization after years of pandemic-era distortion, not a collapse."

- Tanis Read, Managing Broker, Coldwell Banker Horizon Realty

For investors, the focus should remain on quality assets. Modern Class A facilities featuring 32+ foot clear heights, ESFR sprinklers, and proximity to the Highway 401 corridor are consistently outperforming older Class B or C properties. Additionally, small-bay industrial spaces are holding their ground, benefiting from local tenants who are less affected by international trade fluctuations.

These insights underscore a market moving towards disciplined and sustainable growth.

Future Outlook for Industrial Properties

Looking ahead, the industrial sector is poised for steady growth, driven by shifting dynamics in supply chains and inventory strategies. The move from "just-in-time" to "just-in-case" inventory models, combined with ongoing e-commerce expansion, continues to fuel demand. Prime properties are trading at compressed cap rates of 4% to 4.5%, underscoring the sustained confidence of investors.

Keeping an eye on Canada-U.S. trade policies will be crucial. Clarity in trade agreements could unlock latent demand, particularly from manufacturing and steel-reliant tenants in areas like Toronto East. With industrial real estate now making up roughly 45% of total commercial real estate investment in Canada, the sector's fundamentals remain robust for those planning long-term strategies.

FAQs

What cap rate should I expect for prime GTA industrial in 2026?

For prime GTA industrial properties in 2026, cap rates are expected to fall between 3.5% and 4%. This range highlights the market's robust demand and steady resilience, fuelled by strong investor interest and reliable returns.

Which GTA submarkets offer the best risk-adjusted returns in 2026?

Submarkets such as Vaughan, Milton, and Mississauga are projected to deliver some of the strongest risk-adjusted returns by 2026. These regions stand out due to their combination of low vacancy rates, steady demand, high occupancy levels, and a limited supply of industrial properties. This unique mix makes them appealing to investors looking for stable and reliable opportunities.

What building features matter most for power-hungry tenants like data centres?

Power-intensive tenants, like data centres, focus on properties equipped with strong electrical systems, ample power capacity, and dependable infrastructure. These elements are essential to support their high energy demands and maintain continuous operations without disruptions.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist