5 Economic Trends Shaping GTA Industrial Real Estate

5 Economic Trends Shaping GTA Industrial Real Estate

In 2026, the GTA industrial real estate market is shifting after years of rapid growth. Here’s what’s happening:

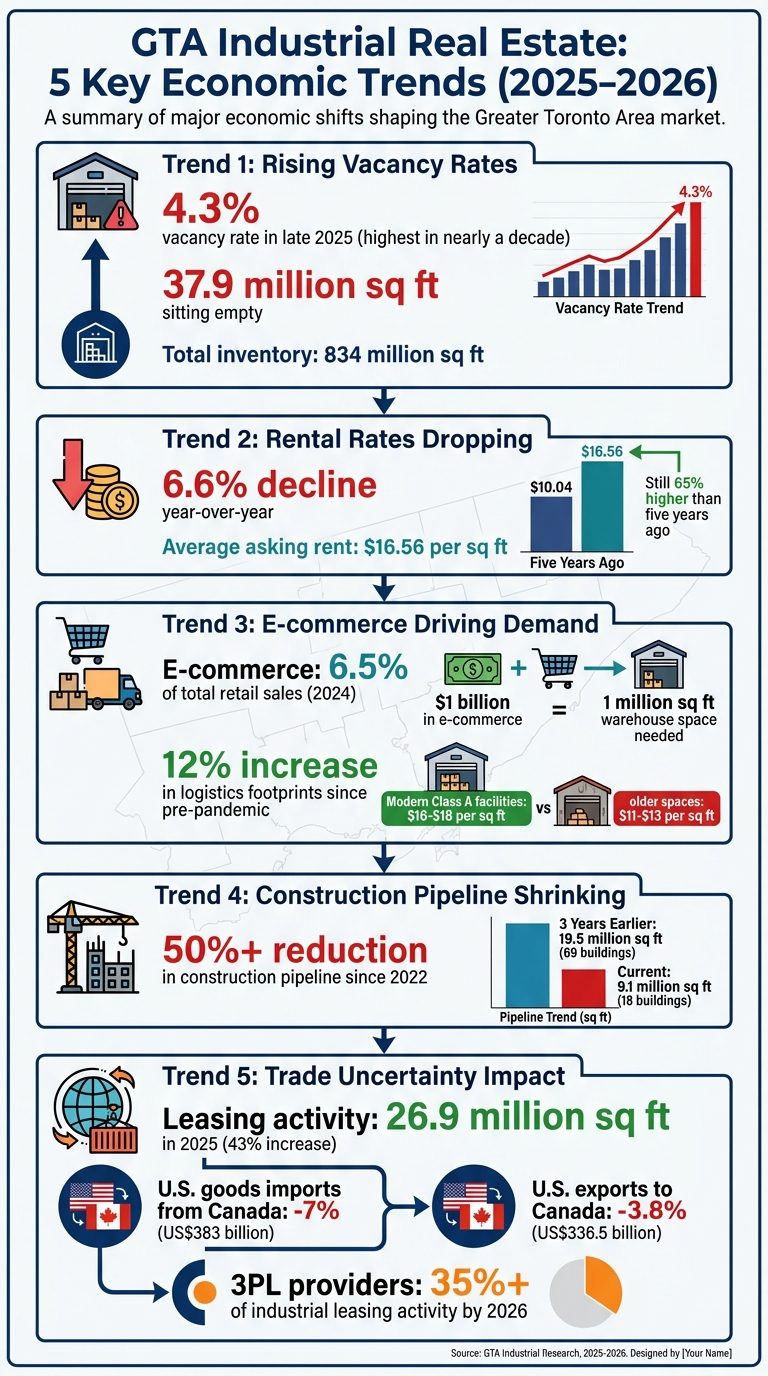

- Vacancy Rates Are Rising: Vacancy rates hit 4.3% in late 2025, the highest in nearly a decade, with 37.9 million square feet sitting empty.

- Rental Rates Are Dropping: Average asking rents fell 6.6% year-over-year to $16.56 per square foot but remain 65% higher than five years ago.

- E-commerce Keeps Driving Demand: Logistics and e-commerce needs, especially from 3PL providers, continue to push demand for modern facilities with features like higher clear heights and advanced infrastructure.

- Oversupply Slows Construction: Developers have cut back on new projects due to oversupply and high costs, with the construction pipeline shrinking by over 50% since 2022.

- Trade Uncertainty Impacts Leasing: U.S. tariff policies are making companies cautious, driving demand for flexible leasing and specialized spaces like cold storage and data centres.

The market is adjusting to more balanced conditions, offering opportunities for tenants to secure favourable lease terms while investors focus on properties with stable cash flow.

GTA Industrial Real Estate Market Trends 2025-2026: Key Statistics

The Definitive Q1 2025 GTA Industrial Report

sbb-itb-1862e65

1. E-commerce and Logistics Demand Growth

E-commerce has completely transformed the way goods move from manufacturers to consumers. Instead of products being stocked on retail shelves, they now travel from manufacturers to fulfilment centres, then to distribution hubs, and finally to customers’ doorsteps. This shift has sparked a surge in demand for specialized logistics services, keeping the need for industrial space across the GTA high, even as vacancy rates have risen.

Third-party logistics (3PL) providers became the main drivers of demand by late 2025. Modern facilities are now expected to include features like 32-foot clear heights, ESFR sprinklers, and large truck courts to support the fast-paced operations of 3PL providers. As Innovative Property Solutions put it:

"By 2026, e-commerce will no longer be a trend. It's just how commerce works, and that reality supports continued strong demand for industrial space across the Toronto area."

The data backs this up. Canadian e-commerce sales accounted for 6.5% of total retail sales in 2024, up from 5.8% in 2023. On top of that, every additional $1 billion in e-commerce sales requires around 1 million square feet of warehouse space. This has led to a 12% increase in logistics footprints since pre-pandemic times.

The push for same-day or next-day delivery has also driven demand for smaller, modern Class A facilities located in key areas like Mississauga, Vaughan, and Richmond Hill. These facilities command higher rents - ranging from $16 to $18 per square foot - compared to older spaces, which rent for $11 to $13 per square foot. The GTA’s location along the Highway 401 freight corridor and its proximity to over half of Canada’s population solidify its role as a key logistics hub. With e-commerce penetration expected to hit 30% by 2030, the demand for strategically located, modern industrial spaces in the GTA is likely to remain strong, even as the broader market slows.

2. Rising Vacancy Rates and Oversupply

The industrial market in the Greater Toronto Area (GTA) is undergoing a noticeable shift, with vacancy rates climbing as absorption slows. E-commerce continues to drive demand in certain niches, but overall, the market is grappling with an oversupply of space. By late 2024, vacancy rates reached a nine-year high of approximately 4.5%, leaving 37.9 million square feet vacant out of a total inventory of 834 million square feet. Although the rate dipped slightly to 4.1% by the end of 2025, with availability at 5.6%, these numbers represent a stark change from the near-full occupancy levels seen in previous years.

This shift is largely tied to a surge in new construction coinciding with a slowdown in demand. Industrial demand hit an 11-year low as businesses pulled back on expansion plans. Rising interest rates, inflation, and trade uncertainties have made companies hesitant to commit to growth. Goran Brelih, Executive Vice President at Cushman & Wakefield, summed it up:

The GTA industrial market is shifting, with vacancy rates at a nine-year high and demand at an 11-year low

The oversupply has also had a noticeable impact on rental rates. GTA North still commands the highest rents at $17.55 per square foot, while GTA East offers the lowest at $15.01 per square foot. Even with a market correction, rents remain 65% higher than five years ago, indicating that landlords are adjusting from peak pricing rather than facing a crash.

In response to these conditions, developers have significantly scaled back new construction. By late 2025, the construction pipeline had dropped to 9.1 million square feet across 18 buildings, down from 19.5 million square feet across 69 buildings just three years earlier. High land acquisition costs from market peaks, coupled with rising material and labour expenses, have made speculative development less appealing. At the same time, sublet listings fell by 27% (1.8 million square feet) in 2025, suggesting that some of the surplus is being absorbed, particularly in secondary spaces. This excess supply has shifted bargaining power toward tenants, who are now benefiting from more flexible lease terms and rental concessions, especially in areas like GTA East where vacancies are highest.

Keith Reading, Senior Director of Research at Morguard, shared a cautiously hopeful perspective:

But if we do see some sort of agreement on trade and trade stability, I think businesses will know what the environment's going to be like, and they can dust off those expansion plans, and we could see economic activity and growth increase toward the end of 2026

These trends highlight the market's adjustment to more balanced conditions after years of extraordinary demand.

3. US Tariff Policies and Trade Uncertainty

US trade tensions have created serious challenges for the Greater Toronto Area (GTA) industrial market. The uncertainty surrounding tariffs has led businesses to rethink how they use warehouse space and manage operations in the region.

In 2025, industrial leasing activity in Toronto reached 26.9 million square feet - a 43% increase from the previous year and the third-highest level ever recorded. However, this surge in leasing activity contrasts sharply with declining trade volumes. U.S. goods imports from Canada fell by 7% to US$383 billion, while American exports to Canada dropped 3.8% to US$336.5 billion. Alan Dewar, Executive Vice-President at GHY International, highlighted the reason behind this discrepancy:

Warehouse demand isn't being driven by growth - it's being driven by uncertainty. Warehouses aren't just storage anymore; they're a front-line tool for managing trade risk

To navigate these challenges, companies are engaging in what some call "trade contortions." This involves rerouting goods through Canadian warehouses and modifying them to meet USMCA exemption criteria. For instance, in early 2026, Lisa McEwan, co-owner of Hemisphere Freight, shared an example where a client shifted their operations. Instead of manufacturing chocolate directly in the U.S., they began importing it from Europe to Canada, processing it into a different product locally. This adjustment made the goods USMCA-compliant, allowing tariff-free entry into the U.S. McEwan noted:

It's companies pivoting to circumvent tariffs

This shifting landscape is not only influencing trade operations but also leading to changes in leasing strategies across the board.

The unpredictability caused by tariffs has made businesses hesitant to commit to long-term leases. Many are now opting for flexible third-party logistics (3PL) solutions. Juana Ross, Research Manager at Cushman & Wakefield, explained:

They would rather avoid a long-term lease obligation at these high rates and prioritize the flexibility of 3PLs more so than the flexibility of having their space themselves

The manufacturing sector is also feeling the strain. Canadian steel exports to the U.S. plummeted by 50% in December 2025 compared to the previous year, while employment in the auto parts industry declined by 9.5%.

These shifts underscore how tariff uncertainty is reshaping both trade and industrial real estate strategies in the region.

4. Growth in Specialized Industrial Properties

As uncertainty continues to shape the market, tenants are increasingly looking for industrial spaces tailored to their changing operational needs. In the Greater Toronto Area (GTA), the industrial market is evolving from traditional warehouses to specialized facilities designed for modern business operations. Key examples include cold storage units, data centres, last-mile distribution hubs, and e-commerce fulfilment centres equipped for advanced logistics.

Cold storage facilities are particularly sought after, driven by the food distribution and pharmaceutical sectors that depend on temperature-controlled environments with precise refrigeration systems. Additionally, food-anchored retail has emerged as a resilient option amidst e-commerce fluctuations, ranking as the top product/market combination in Toronto during Q4 2025. At the same time, the demand for data centres is climbing as businesses invest in strengthening their digital infrastructure.

This shift reflects a broader trend often referred to as a "flight-to-quality." Tenants are moving away from older Class B and C properties in favour of modern Class A facilities. These newer spaces typically feature taller clear heights (around 32 feet) and enhanced power capabilities, making them ideal for advanced technologies and automation. Class A warehouses in the GTA command higher rents, ranging from $16–$18 per square foot, compared to $11–$13 for older facilities. CBRE notes:

New leasing activity will be driven by a flight to quality to take advantage of taller clear heights and stronger power or outsource their distribution operations to 3PL providers

Developers are also transforming older properties into data centres and hybrid industrial-retail spaces. Third-party logistics providers (3PLs) are playing a significant role in this market, projected to account for over 35% of all industrial leasing activity by 2026.

With speculative development expected to stay limited in 2026, the market is leaning towards build-to-suit projects. These custom-built spaces allow businesses to secure properties designed specifically for their needs. Features include enhanced power infrastructure for digital operations, specialized refrigeration for cold storage, and strategically located last-mile facilities sized between 30,000 and 100,000 square feet. This trend highlights the growing demand for spaces that align with modern logistics and operational requirements.

For businesses seeking expert guidance in navigating this changing landscape, Lennard Commercial – Industrial Real Estate Services offers insights and tailored solutions based on deep market knowledge and proprietary data, helping companies succeed in Toronto and the GTA.

5. Economic Slowdown and Declining Rental Rates

The broader economic slowdown, coupled with rising vacancies and trade uncertainties, is now making its mark on rental trends. By Q4 2025, the average asking net rental rate across the GTA dropped to $16.56 per square foot, reflecting a 6.6% year-over-year decline. This is a notable shift from the market's peak in 2023, when rents averaged $16.84 per square foot. However, even with this dip, current rates remain higher than pre-pandemic levels, highlighting the long-term changes in the market.

This drop in rental rates can be attributed to both increased supply and reduced demand. Factors like high interest rates, ongoing inflation, and global trade uncertainties have led many businesses to hit pause on their expansion plans. Victor Cotic, Executive Vice President at Colliers, explains the cautious approach investors are now taking:

Industrial rents have begun to 'cool'... investors are currently more cautious when assessing industrial investment opportunities that have near-term expiries and leasing risk.

This shift in investor sentiment is evident in the numbers. Industrial investment activity in the GTA saw a 4% year-over-year decline, totalling $5.3 billion by the end of 2025. These trends underline a broader market transition that favours tenants over landlords.

For tenants, this changing landscape has brought new opportunities. Landlords, eager to fill vacant spaces, are adopting aggressive leasing strategies. These include offering concessions, enhanced tenant-improvement allowances, and even free rent periods. Goran Brelih, Executive Vice President at Cushman & Wakefield, highlights this trend:

Rising vacancy may require more aggressive leasing strategies, such as rental concessions or flexible terms, to attract tenants in a softening market.

CBRE's 2026 market outlook echoes this sentiment, noting that lease renewals - especially for office and industrial spaces - are increasingly coming with tenant-friendly terms like higher tenant-improvement allowances and extended free rent periods. For businesses, particularly in high-vacancy areas like GTA East (where rents average $15.01 per square foot), this is a golden opportunity to negotiate better lease agreements.

Looking ahead, rental rates could begin to stabilize by late 2026 as the construction pipeline has slowed significantly. This reduced supply may eventually drive rents upward again. For now, though, tenants remain in the driver’s seat, with plenty of room to secure favourable terms.

GTA Industrial Market Comparison by Submarket

Industrial market dynamics across the GTA submarkets vary significantly. While the overall vacancy rate rose to 4.1% in Q4 2025, each submarket tells a different story. The West and North submarkets, which include Brampton, Mississauga, and Vaughan, consistently maintain vacancy rates below the GTA average. Brampton reported a 2.8% vacancy rate, Mississauga stood at 3.1%, and Vaughan recorded 2.9%. These areas remain highly desirable due to their proximity to the Highway 401 corridor and Pearson Airport. Such low vacancy rates continue to support higher rental prices in these sought-after locations.

Rental rates in these high-demand areas reflect their appeal. Vaughan leads with $20.00 per square foot, followed by Mississauga at $19.25 per square foot and Brampton at $18.75 per square foot. Year-over-year rent growth in these submarkets ranged between 10% and 12% heading into 2025, driven largely by the surge in logistics and e-commerce demand. Third-party logistics (3PL) providers and supply chain operators remain key players, particularly in Brampton and Mississauga.

In contrast, outer markets like Caledon and Milton in the West offer a different dynamic. With a 3.5% vacancy rate and average rents of $18.00 per square foot, these areas attract large-scale distribution centres seeking more cost-effective options. However, these regions are absorbing surplus inventory from the 2021–2022 development boom, especially in large-bay warehouse and logistics properties. This oversupply has led to higher vacancy rates in outer markets compared to the tighter conditions in the Central and North submarkets.

Shifting occupier needs are also reshaping smaller property segments. Spaces under 50,000 square feet are experiencing higher vacancy across all submarkets. This trend reflects a broader market adjustment as tenants reassess their space needs in light of rising costs and increased supply. With availability reaching 5.6% across the GTA, tenants now have more negotiating power than they've seen in years.

These market contrasts give tenants a chance to capitalise on local conditions. While premium locations like Vaughan and Mississauga maintain higher rents and tighter vacancy, the overall market softening has opened up opportunities, particularly in areas where new supply has exceeded immediate demand.

Conclusion

The Greater Toronto Area (GTA) industrial real estate market is undergoing significant changes, shaped by five key trends: the expansion of e-commerce, increasing vacancy rates, trade uncertainties, demand for specialized properties, and declining rental rates. These factors are driving the market toward a post-pandemic equilibrium. While rental rates have cooled and availability has climbed to 5.0% by late 2025, property valuations have shown resilience. The average sale price of $275 per square foot is only 7% below the 2023 peak, reflecting continued investor trust in the sector's long-term outlook.

Institutional investors are playing a larger role, now making up 45% of purchases in 2025, a sharp rise from under 20% in 2024. This indicates a growing preference for Class A properties with dependable cash flow. As Victor Cotic from Colliers highlights:

The GTA industrial investment market remains resilient in 2025... cash flow is now king

A notable slowdown in new construction is also reshaping the market. Deliveries have dropped from 17.0 million square feet in 2023 to 11.1 million square feet in 2025, which is expected to result in a supply shortage by late 2026 and into 2027. Positive absorption levels, reaching 4.1 million square feet in Q4 2025, further point to a market that may soon shift back in favour of landlords. Drew Rider from Colliers remarks:

The market is stabilizing, and 2026 is shaping up with cautious optimism

This evolving landscape presents opportunities for both tenants and investors. Tenants can leverage current high availability and flexible lease terms to secure deals before the construction slowdown tightens supply. Meanwhile, investors focusing on replacement value and immediate cash flow may find this period ideal for acquiring high-quality assets, poised to benefit from an expected rental increase in 2027.

FAQs

Does rising vacancy mean it’s a good time to renegotiate my industrial lease?

Higher vacancy rates can create a chance to renegotiate your industrial lease. When there's more availability in the market, landlords are often more flexible, which could give you an edge during negotiations.

Which GTA submarkets are most likely to rebound first if supply tightens in 2027?

Submarkets within established industrial corridors in the Greater Toronto Area (GTA) that have consistently seen low vacancy rates and high demand are expected to recover first if supply becomes constrained in 2027. While no specific submarkets are named, these areas typically feature steady industrial activity and limited space availability.

How should tariff uncertainty affect my warehouse leasing strategy?

Tariff uncertainty demands careful planning when it comes to leasing decisions. Prioritizing flexible lease terms can help you adjust to unexpected trade disruptions. Pair this with a detailed market analysis to better understand potential risks. Together, these steps can help you stay nimble in an ever-changing economic environment.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist