GTA Industrial Rental Rates: 10-Year Trends

GTA Industrial Rental Rates: 10-Year Trends

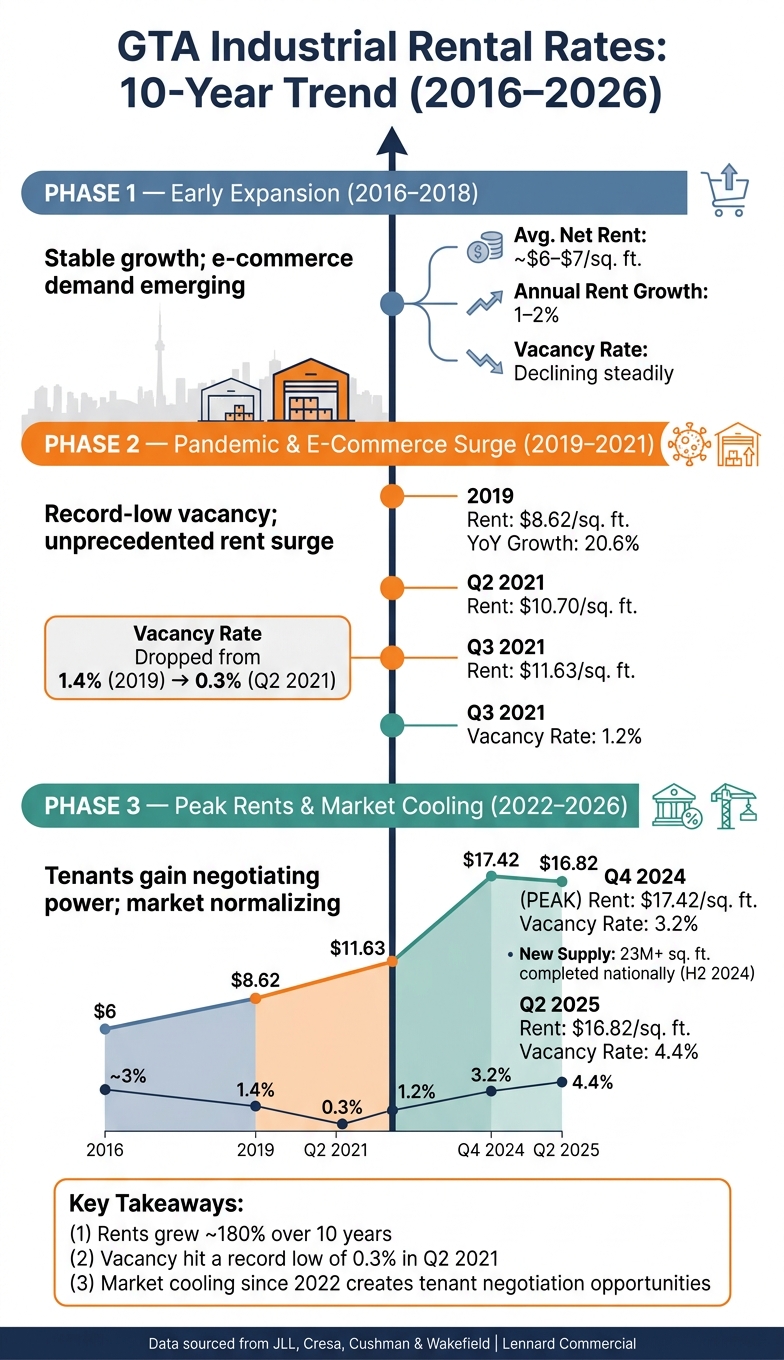

GTA industrial rental rates have experienced dramatic shifts over the past decade, reflecting changes in demand, supply constraints, and broader economic factors. Here's a quick summary of the key trends:

- 2016–2018: Rents grew modestly (~1–2% annually), with rates around $6–$7/sq. ft. Limited industrial land and growing e-commerce demand began tightening the market.

- 2019–2021: Demand surged due to e-commerce and pandemic disruptions. Rents rose sharply (20.6% YoY in 2019), reaching $11.63/sq. ft. by Q3 2021. Vacancy rates hit record lows (0.3% in Q2 2021).

- 2022–2026: Rents peaked at $17.42/sq. ft. by Q4 2024, driven by supply shortages and high demand. However, new developments and rising interest rates cooled the market, with vacancy rates increasing to 4.4% by mid-2025.

Key Takeaways:

- E-commerce growth and population increases fuelled demand for modern facilities.

- Supply constraints and zoning challenges limited new developments, keeping vacancy rates tight.

- Market cooling since 2022 gave tenants more negotiating power, with landlords offering incentives like free rent periods.

For tenants, the current environment offers negotiation opportunities. For investors, focusing on modern Class A facilities in key locations remains a strong strategy.

GTA Industrial Rental Rates: 10-Year Trend (2016–2026)

GTA Industrial Rental Rate Trends by Phase (2016–2026)

Early Expansion Phase (2016–2018)

In 2016, the GTA industrial market was relatively stable. Annual rent growth hovered between 1% and 2%, with national year-over-year increases of just 1.4% in Q2 2016 and 1.1% by Q4 2016. This period followed the economic adjustments caused by the 2014 oil price crash, which had slowed commercial real estate activity across Canada.

During this time, e-commerce began reshaping demand. Major retailers and logistics giants like Amazon, Costco, and Walmart expanded their distribution networks. However, the GTA faced limited zoned and serviced industrial land, and lengthy municipal approvals further slowed new developments. Vacancy rates started to decline steadily, setting the stage for what would soon become one of the tightest industrial markets in history. These modest but steady trends laid the groundwork for a dramatic shift during the pandemic years.

Pandemic and E-Commerce Surge (2019–2021)

By 2019, the GTA industrial market had shifted into high gear. Average rents surged 20.6% year-over-year, reaching $8.62 per sq. ft., while the vacancy rate dropped to a record low of 1.4%. Then came the pandemic, which only accelerated these trends.

With lockdowns in place, consumer spending moved online at an unprecedented pace. Businesses scrambled to secure warehouse space to manage supply chain disruptions and stockpile inventory. By Q2 2021, the GTA vacancy rate had plummeted to just 0.3%, and average net asking rents climbed to $10.70 per sq. ft. in the same quarter. Developers, dealing with rising construction costs, delayed lease agreements to capitalize on even higher rents. As Cresa observed:

"The Greater Toronto Area (GTA) industrial market continued to reach unfathomable heights this quarter as average net asking rents increased to $10.70 per square foot."

This surge in demand and pricing set the market on a trajectory that would peak in the years following the pandemic.

Peak Rents and Market Cooling (2022–2026)

After the pandemic-fuelled boom, the market hit its peak in the years that followed. By Q3 2021, average net rents had climbed to $11.63 per sq. ft., with vacancy still at a tight 1.2%. High-profile leases highlighted this demand surge: Amazon finalized a 1.05-million sq. ft. distribution centre in Ajax, and H&M secured a 716,000 sq. ft. lease at the GTA East Industrial Park.

Starting in 2022, the Bank of Canada's interest rate hikes began to cool investor enthusiasm and slow new development. However, the construction pipeline from the peak years continued to deliver. By the second half of 2024, over 23 million sq. ft. of new industrial space had been completed nationwide. As a result, GTA vacancy rates rose to 3.2% by Q4 2024, and availability rates increased from 4.3% to 4.7% in the same quarter. Despite these adjustments, average net rents reached $17.42 per sq. ft. by the end of 2024, underscoring the sharp repricing of the market over the previous decade.

| Phase | Period | Avg. Net Rent | GTA Vacancy Rate |

|---|---|---|---|

| Early Expansion | 2016–2018 | ~$6–$7/sq. ft. (est.) | Declining toward 1.4% |

| Pandemic Surge | 2019–Q3 2021 | $8.62 → $11.63/sq. ft. | 1.4% → 0.3% |

| Peak & Cooling | Q4 2021–Q4 2024 | $11.63 → $17.42/sq. ft. | 1.2% → 3.2% |

sbb-itb-1862e65

Key Drivers Behind GTA Industrial Rent Changes

Demand-Side Factors

Over the past decade, e-commerce has been a major force driving demand for industrial space in the GTA. This trend, which was already gaining momentum, accelerated significantly during the COVID-19 pandemic as consumer habits shifted rapidly. Retail giants like Amazon, Costco, and Walmart responded by expanding their distribution networks. For instance, by mid-2023, Amazon had added approximately 4.8 million sq. ft. of warehouse space in Canada, with plans to reach about 28.3 million sq. ft. by the end of 2024.

The Toronto CMA’s population growth also contributed to this demand. Between 2016 and 2021, the region grew by roughly 10%. However, by 2025–2026, net absorption began to slow as major tenants approached the maturity of their distribution networks. Despite the cooling absorption rates, developers continued to face challenges in meeting the robust demand for industrial space.

Supply Constraints and Land Availability

The surge in demand only tells part of the story - limited supply has been a critical factor driving rent increases. As JLL highlighted:

"Bringing planned product to market at a rapid pace continues to be difficult. Scarcity of zoned and serviced land and lengthy municipal approval processes have continued to challenge developers."

This lack of available land pushed tenants to consider fringe areas like Ajax and Oshawa in the GTA East. At the same time, infill redevelopment projects gained popularity, such as the 337,200 sq. ft. speculative redevelopment at 541 Kipling Ave. The supply shortage was so severe that up to 95% of new industrial completions were pre-leased before construction even finished.

Capital Markets and Infrastructure Influences

Financial conditions and infrastructure developments have also played a significant role in shaping the industrial rent landscape. Historically low interest rates through 2021 drove cap rates to record lows - 3.8% for single-tenant properties and 4.1% for multi-tenant properties by late 2021. This environment spurred unprecedented investment activity, with the sector seeing a record $5.4 billion in transactions by Q3 2021.

However, when the Bank of Canada began raising interest rates aggressively in 2022, market conditions shifted. Cap rates rose by approximately 100–150 basis points. As noted by one market analysis:

"Higher interest rates (as of 2025) have begun to normalize cap rates upward by roughly 100–150 bps in many markets. This tends to cap how much landlords can raise rents."

Infrastructure also played a key role. Access to major highway corridors in the GTA East allowed fringe submarkets to take on the demand that core areas could no longer accommodate. These financial and logistical factors intertwined with broader market trends, shaping rental rates and tenant strategies over the years.

What GTA Industrial Rent Trends Mean for Tenants and Investors

Tenant Considerations

The GTA industrial market has shifted significantly since its peak in 2021–2022, creating a more tenant-friendly environment. Vacancy rates have climbed from just 1.2% in Q3 2021 to 4.4% by Q2 2025, giving tenants more room to negotiate favourable terms.

Industrial broker Joe Rosati summed it up well:

"Tenants that are active in the market are finding improved negotiating leverage."

Landlords, who once had waiting lists for their properties, are now offering incentives like free rent periods, tenant improvement allowances, and more flexible leases to attract occupants. For tenants whose leases are up for renewal in 2025–2026, the timing couldn't be better. Average asking net rents have dropped from their 2024 high of $18.11 per square foot to $16.82 per square foot by Q2 2025. While these rates are still higher than pre-COVID levels, the downward trend is working in tenants' favour.

While tenants enjoy these new opportunities, the changing market dynamics also bring unique challenges and opportunities for property owners and investors.

Owner and Investor Insights

For property owners, the current market offers a mix of challenges and opportunities. Those with leases signed in 2019–2020, when rents averaged around $8.62 per square foot, now have a chance to renegotiate leases at higher rates, even though rents have softened slightly compared to their peak.

On the investment side, activity has slowed. The average industrial sale price fell from $358 per square foot in Q1 2025 to $339 per square foot in Q2 2025. However, most industrial property owners in the GTA are financially stable, with limited debt exposure. This stability allows them to hold firm on pricing rather than resort to steep discounts.

Goran Brelih, Senior Vice President at Cushman & Wakefield, offered a long-term perspective:

"Now that we seem to be caught in a supply trap, one should expect to see values increase further, albeit at a decelerating pace relative to the jump we saw over the past 5 years."

For investors, the key lies in distinguishing between asset classes. Modern Class A logistics facilities, often occupied by e-commerce tenants, remain highly desirable. In contrast, older Class B and C properties face growing challenges as tenants prioritize efficiency and prime locations.

The Role of Specialized Advisory Services

In a market defined by fluctuating rents and shifting dynamics, expert guidance is more critical than ever. Successfully navigating lease renewals, relocations, or acquisitions requires precise timing and a deep understanding of market trends.

Michael Law of Lennard Commercial, who specializes in industrial real estate across Toronto and the GTA, offers tailored advice for both tenants and property owners. His expertise in areas like lease renewals, investment sales, and acquisitions - combined with access to proprietary market data - enables clients to secure better deals. Whether it's finding a logistics facility in Brampton or evaluating a multi-tenant property in the GTA East corridor, having a trusted advisor can make all the difference in a rapidly changing market.

Conclusion: 10 Years of GTA Industrial Rental Rate Changes

Key Takeaways from the 10-Year Analysis

The GTA industrial market has experienced a remarkable transformation over the past decade, marked by three distinct phases. Initially, rental rates grew modestly at 1–2% annually. Then, 2019 saw a dramatic 20.6% surge, pushing rates to $8.62 per square foot. By early 2025, rates are projected to reach $25–$26 per square foot, fuelled by the rise of e-commerce, limited land availability, and persistently low vacancy rates.

A closer look reveals the enduring factors behind this growth. Amazon's expanding logistics operations in Canada have significantly reshaped the demand for industrial space, highlighting a broader shift towards e-commerce-driven distribution. Additionally, tenants have increasingly gravitated toward modern facilities with high ceilings, leaving older properties behind.

"Industrial is definitively being fuelled by E-commerce demand, as well as other verticals such as online grocery sale, transportation, and even film production." - Goran Brelih, Senior Vice President, Cushman & Wakefield ULC

However, the market has recently shown signs of adjustment. In Q2 2024, national industrial asking rents saw a 2.1% year-over-year decline - the first in 12 years - indicating a potential shift toward normalization.

These trends provide valuable context for understanding the evolving GTA industrial market.

What to Watch Going Forward

Looking ahead, several factors will shape the market's trajectory. One of the most critical is the absorption of over 23 million square feet of new industrial space introduced in the latter half of 2024. If demand keeps pace with this influx, vacancy rates could stabilise, and rental rates may hold steady. However, slower absorption might give tenants an opportunity to negotiate more favourable lease terms. At the same time, rising rental rates could limit further value growth, given the ongoing scarcity of zoned industrial land.

For tenants, early planning is key. Those with leases in modern, well-located facilities should begin renewal discussions 18 to 24 months in advance. For investors, targeting properties with near-term lease expirations could allow them to capitalise on the significant rent increases seen since 2019.

For more tailored advice, reach out to Michael Law at Lennard Commercial - Industrial Real Estate Services.

GTA Industrial Market Update | Q4 2024 | Cresa Toronto

FAQs

What’s the difference between vacancy and availability rates?

Vacancy rate refers to the percentage of industrial space that is currently unoccupied and ready for immediate lease or purchase. On the other hand, the availability rate takes a broader view, including not just vacant units but also spaces under construction and pre-leased spaces that are not yet occupied.

To put it simply: vacancy rate highlights unoccupied space available right now, while availability rate accounts for all space that could eventually be leased.

How do interest rates affect GTA industrial rents and cap rates?

Higher interest rates tend to push cap rates up and bring rental rates down in the Greater Toronto Area (GTA) industrial market. This combination usually results in lower property values and more affordable rents. On the flip side, when interest rates drop - like the recent cuts introduced by the Bank of Canada - it often triggers cap rate compression and drives property values higher.

How far in advance should I start an industrial lease renewal in the GTA?

Starting the industrial lease renewal process in the GTA around 9 to 12 months before your lease expires is a smart move. This timeline gives you enough room to carefully plan, negotiate new terms, and make any adjustments needed to align with your business goals.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist