Industrial Lease Renewal: 7 Steps to Negotiate Better Terms

Industrial Lease Renewal: 7 Steps to Negotiate Better Terms

Renewing your industrial lease is a chance to save money, improve terms, and secure flexibility for your business. Landlords prefer keeping reliable tenants, as replacing them can be costly and time-consuming. With industrial rents rising in Canada and vacancy rates increasing, tenants have leverage if they start early and approach negotiations strategically.

Key Takeaways:

- Start Early: Begin planning 18–24 months before your lease expires.

- Review Your Lease: Understand renewal clauses, deadlines, and rent calculation methods.

- Assess Your Needs: Check if your current space aligns with your future business goals.

- Research Alternatives: Explore market trends and comparable properties to strengthen your position.

- Negotiate Terms: Focus on rent, tenant improvement allowances, and caps on operating costs.

- Get Expert Help: Work with real estate professionals and legal advisors to finalize the agreement.

7-Step Industrial Lease Renewal Negotiation Process

Commercial Lease Negotiation Tactics: How to Save $$$

sbb-itb-1862e65

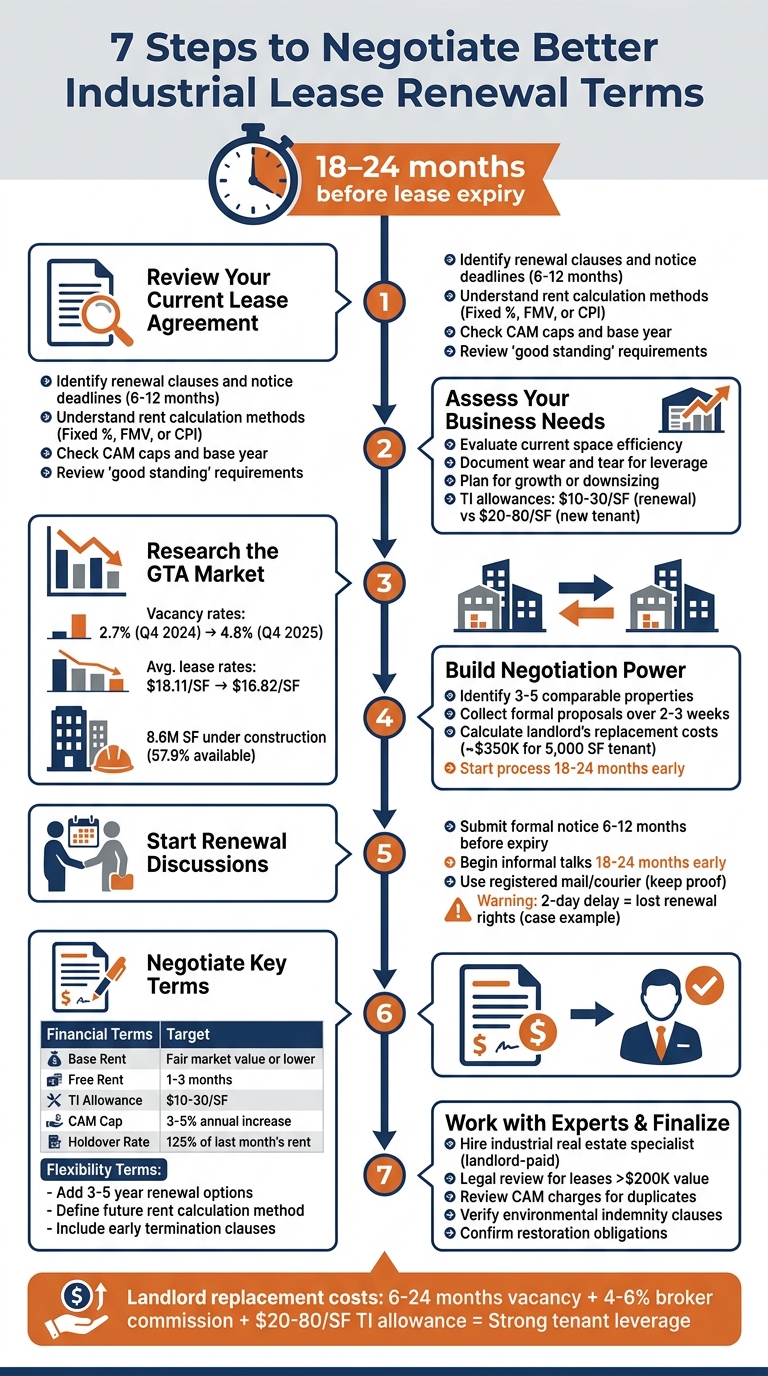

Step 1: Review Your Current Lease Agreement

Before contacting your landlord, take the time to carefully review your lease agreement. This document is the backbone of your negotiation, outlining your rights, deadlines, and how your renewal rent will be calculated.

Don’t rely on memory or assumptions. The lease includes critical renewal clauses, and even a small oversight can have major consequences. For instance, in 2324702 Ontario Inc. v. 1305 Dundas W Inc., a mere two-day delay cost the tenant their renewal rights.

Identify Key Renewal Clauses

Start by locating the "Option to Renew" clause in your lease. This section specifies when and how you must notify your landlord if you intend to renew. Many industrial leases require written notice 6–12 months before the lease ends, and they often dictate the delivery method - registered mail, courier, or even email. Using the wrong method could invalidate your notice.

Check for any conditions tied to renewal. For example, some leases require you to be in "good standing", meaning you’ve paid rent on time and avoided property damage. If there have been any issues during your current term, address them before entering renewal discussions. Also, confirm whether your lease allows for multiple renewals (e.g., two five-year terms) or just one.

"Missing these deadlines can have severe consequences. Canadian courts have consistently upheld strict compliance with renewal notice periods." - CHI Real Estate Group

To avoid missing deadlines in the future, consider negotiating a "reminder notice" clause, requiring your landlord to notify you as the renewal date approaches.

Understand How Rent Increases Are Calculated

After clarifying renewal deadlines and conditions, focus on how rent adjustments are handled in your lease.

Your lease should outline the method for calculating renewal rent. The three most common approaches are:

- Fixed percentage increases: For example, a 3% annual increase. This provides predictability but could exceed market rates if conditions soften.

- Fair Market Value (FMV): Rent is adjusted based on comparable properties. While this aligns with current market conditions, it can lead to uncertainty and, in a strong market, significant rent hikes.

- Consumer Price Index (CPI) adjustments: Rent is tied to inflation rates. This may be a more favourable option as inflation is expected to moderate by 2025–2026.

If FMV is used, look closely at how "comparables" are defined. Ensure the lease specifies which property types are included and excludes any value added by your tenant improvements.

Also, review your "Additional Rent" provisions, which cover expenses like property taxes, insurance, and common area maintenance (CAM). Check whether there’s a cap on CAM increases and confirm the base year. If your lease has an outdated CAM cap, negotiate to reset it to current levels with a reasonable 3–5% annual cap. This is especially important as nearly half of Canadian businesses report rising insurance and maintenance costs as a major concern.

Step 2: Assess Your Business Needs and Space Requirements

Once you've confirmed your lease details, it's time to take a closer look at whether your current space still aligns with your evolving business needs.

What worked when you first signed the lease might not be as effective now. Before you dive into renewal discussions, think about whether the property still supports your goals for the next three to five years. This includes looking at not just the size but also the efficiency of the space, its ability to accommodate growth, and any upgrades it might need. Start this process well before your lease expires to keep your options open.

Review How You Use Your Current Space

Take a hard look at how your current layout supports your operations. Are there areas where workflows are getting bogged down? This can happen if you've added things like e-commerce fulfilment, expanded delivery services, or introduced specialized production areas.

Also, don’t overlook visible wear and tear. Things like old flooring, outdated lighting, or peeling paint might seem minor, but they can be useful when negotiating. A worn-out space gives you leverage to ask for a Tenant Improvement (TI) allowance during renewal. For context, landlords typically offer $10–$30 per square foot for a "refresh", compared to $20–$80 per square foot for new tenants. These allowances not only improve your space but also highlight the value of keeping existing tenants.

Don’t forget to assess your building systems. If HVAC, electrical setups, or loading docks are nearing the end of their lifespan, it could mean higher maintenance costs or even operational disruptions. Nearly half of Canadian businesses have reported that rising maintenance and insurance costs are a top concern. Documenting these issues can strengthen your case for landlord-funded upgrades.

Plan for Business Growth or Changes

Think ahead about how your space needs might change. Whether you're planning to expand, downsize, or maintain your current footprint, projecting future requirements is key. Keep in mind that industrial space in Canada is competitive, with national availability sitting at around 6% as of early 2025. If growth is on the horizon, consider negotiating expansion rights, like a Right of First Refusal on nearby space.

"Your space needs may change over time. When negotiating renewal options, consider including rights to expand or contract your premises at predetermined points." - CHI Real Estate Group

If your business model is shifting - say, adding omnichannel capabilities or creating dedicated pickup areas - figure out what layout changes could boost efficiency. Use this as an opportunity to request a TI allowance to fund those changes. For example, replacing a 5,000-square-foot tenant could cost a landlord roughly $350,000, factoring in vacancy and commissions. This gives you plenty of leverage to negotiate improvements that benefit both sides.

Lastly, aim for flexibility. Options like multiple shorter consecutive terms - such as two three-year renewals - can help you adapt to future changes.

With a clear understanding of your space and operational needs, you're ready to explore the competitive industrial market in the GTA in the next step.

Step 3: Research the GTA Industrial Real Estate Market

It’s time to gather solid market data to back up your lease renewal discussions.

The GTA industrial real estate market has been showing signs of softening, which works in favour of tenants during negotiations. For example, vacancy rates climbed from 2.7% in Q4 2024 to 4.4% by Q2 2025, eventually reaching 4.8% in Q4 2025. At the same time, average asking net lease rates fell from their peak of $18.11 per square foot to $16.82 per square foot over four consecutive quarters. Properties are staying on the market longer, and landlords are offering more concessions to attract tenants. In particular, large-bay spaces in the GTA West and East have seen a rise in availability due to new developments.

"With more options available and landlord expectations beginning to reset, tenants that are active in the market are finding improved negotiating leverage." - Joe Rosati, Industrial Real Estate Specialist

Adding to this dynamic, about 8.6 million square feet of industrial space was under construction by the end of 2025, with 57.9% still available for lease. When new builds struggle to find tenants, existing landlords often feel pressured to compete by offering better pricing or terms. This is valuable leverage you can use during your discussions.

Use Comparable Lease Data

While general market trends provide helpful context, specific lease comparables are essential for strengthening your renewal strategy. These lease comps include detailed information about recent agreements for similar properties, such as base rent, escalation rates, tenant improvement allowances, and landlord concessions.

Platforms like CompStak and relationships with commercial brokers are excellent sources for this data. Brokers, in particular, often have access to the most up-to-date information. Focus on lease deals within the past year in your submarket, prioritizing properties similar in size, ceiling height, loading capabilities, and location. This allows you to identify key benchmarks to guide your negotiations.

"Lease comps provide a window into prevailing rental rates, concessions, and lease structures across similar commercial properties." - CompStak

Look at metrics like average starting rent, typical escalation rates, tenant improvement allowances, and any rent-free periods. These details help you make a strong, evidence-based case during discussions. Don’t underestimate the value of informal insights either - talking with neighbouring businesses can uncover useful information. Combining these informal observations with formal lease data gives you a well-rounded understanding that landlords will find difficult to challenge.

Armed with this market knowledge, you’ll be better prepared to evaluate alternative options and strengthen your position at the negotiation table.

Step 4: Build Negotiation Power with Alternative Options

After gathering solid market insights in Step 3, it’s time to strengthen your position by exploring alternative properties. Even if you plan to stay in your current space, researching comparable options can give you a stronger hand at the negotiation table. When landlords see that you have realistic alternatives, they’re more likely to offer better rental rates, greater concessions, or more tenant-friendly lease terms.

Shifting the conversation from a one-on-one negotiation to a competitive market scenario changes the dynamics. Without alternatives, your leverage is limited. However, presenting formal proposals from other properties can significantly improve your bargaining position.

"The goal, then, is not simply to find a better deal elsewhere. It is to construct a process in which the threat of moving is real enough that staying becomes the landlord's problem to solve." - Gordon Lamphere J.D., Licensed Real Estate Broker, Van Vlissingen and Co.

Another key tactic is understanding your landlord’s costs for replacing you as a tenant. Demonstrating how much more expensive it would be for them to find a new tenant can make renewing your lease a more appealing option for them.

Find Alternative Industrial Properties

Start by identifying 3–5 comparable properties that meet your business needs. Look at factors like clear heights, loading dock availability, power capacity, and zoning. Over a period of 2–3 weeks, reach out to these landlords and request formal proposals. These should include details like base rent, tenant improvement (TI) allowances, rent-free periods, and operating expenses. Collecting these proposals creates competitive pressure while keeping your intentions discreet.

Once you have these offers, they become invaluable tools in negotiations with your current landlord. For example, you could present a proposal highlighting a rate of "$X per square foot with $Y TI allowance" to illustrate the kind of deal you could get elsewhere.

Given that sublease availability in the Greater Toronto Area exceeded 7 million square feet in late 2025 and vacancy rates stood at 4.2% in Q3 2025, there’s a good chance you’ll find several viable alternatives. Whether you ultimately decide to stay or move, having these options gives you the leverage to negotiate better terms.

Start the Process 18–24 Months Early

Timing plays a critical role in this process. Begin your market research and initial discussions at least 18–24 months before your lease expires. This is well before the formal notice period, which usually starts 6–12 months before expiry. Starting early gives you enough time to tour properties, gather proposals, and negotiate letters of intent without feeling rushed.

It also ensures you don’t miss renewal deadlines, which can be costly. In the case of 2324702 Ontario Inc. v. 1305 Dundas W Inc., a tenant lost their renewal rights entirely after missing the notice deadline by just two days. The court ruled that the landlord had no obligation to accept the late notice.

"Running out the clock on a renewal option before exploring alternatives is one of the most common and costly mistakes industrial tenants make." - Van Vlissingen and Co.

Step 5: Start Renewal Discussions with Your Landlord

Now that you've gathered market research and explored alternatives, it's time to focus on opening discussions with your landlord. Timing and approach are everything here. Your goal is to safeguard your renewal rights while keeping your leverage intact through a professional and strategic approach.

Submit Renewal Notice on Time

Most leases require formal written notice 6–12 months before the lease expires. Missing this deadline - even by a single day - can cost you your renewal rights. For example, in one case, a tenant lost their renewal rights because their notice was submitted just two days late.

To avoid this, set calendar reminders well in advance. When you're ready to submit the notice, follow the exact delivery method outlined in your lease - whether that's through registered mail, courier, or another specified method. Always keep proof of delivery. During negotiations, you might also want to ask for a "reminder notice" clause, which would require your landlord to notify you of future renewal deadlines.

Begin Informal Conversations Early

Start informal discussions with your landlord 18–24 months before your lease expires. These early conversations are a chance to address maintenance issues, clarify rent calculation methods, and get a sense of your landlord's long-term plans. Be cautious, though - avoid committing to a renewal too soon. Instead, frame these talks as part of a broader market evaluation to ensure your current lease terms remain competitive.

This strategy keeps your leverage intact while showing that you're a reliable tenant - something landlords value. Keep in mind that replacing a tenant comes with costs for landlords, like potential vacancies or marketing expenses, which works in your favour during negotiations. These early discussions also give you time to address any property concerns, smoothing the path for formal negotiations later on.

"The landlord's real alternative to renewing your lease is not the next tenant at market rent - it is a vacancy that will sit on the market for months." - Lextract

Step 6: Negotiate Key Lease Terms

As discussions progress, focus on negotiating lease terms that can help lower your costs and provide greater flexibility. Use the market data and alternative options you've gathered to strengthen your position.

Negotiate Financial Terms

Start by addressing the base rent, then move on to other financial concessions. If your market research shows you're paying above-average rates, use that data to support your case. For instance, if comparable properties in your area lease for $12 per square foot and you're paying $15, this difference can be a compelling argument to request a reduction.

Beyond base rent, free rent periods can be a game-changer. Requesting 1–3 months of rent abatement can significantly reduce your overall occupancy costs without forcing your landlord to deal with the hassle of finding a new tenant.

Another key area to discuss is the tenant improvement (TI) allowance. Aim for $10–$30 per square foot to fund necessary updates to your space. Present this as a win-win: it refreshes your space while maintaining or even boosting the value of the landlord's property.

Also, look at common area maintenance (CAM) caps. Propose capping annual increases at 3–5% to avoid unexpected spikes in operating costs. Additionally, address holdover rates. If your lease includes penalties of 150–200% of your last month's rent for staying past the lease term, negotiate to reduce this to around 125% for more flexibility during transitions.

Here’s a quick reference table to guide your renewal targets:

| Financial Term | Typical Renewal Target | Market Support Data to Use |

|---|---|---|

| Base Rent | Fair market value or lower | Comparable lease rates and current vacancy rates |

| Free Rent | 1–3 months | Landlord's estimated downtime (6–24 months) |

| TI Allowance | $10–$30/SF (refresh) | Comparable TI figures from recent leases |

| CAM Cap | 3–5% annual increase | Historical CAM trends and submarket averages |

| Holdover Rate | 125% of last month's rent | Standard market concessions for reliable tenants |

Once you've addressed these financial terms, shift your focus to long-term flexibility.

Request Flexibility and Future Renewal Options

After securing financial concessions, negotiate terms that allow for future adaptability. If your current lease lacks renewal options, seek to add 3–5 year renewal terms. Without these, you risk becoming a holdover tenant with fewer rights once your lease ends.

Be clear about how future rent will be determined in these renewal terms. Specify whether it will involve a fixed percentage increase, a tie to the Consumer Price Index (CPI), or another defined method like arbitration. Avoid vague terms like "market rent", which can leave you vulnerable to unpredictable cost increases.

If your business's future is uncertain, consider adding early termination clauses or provisions for assignment and subletting. These options can serve as an exit strategy if your circumstances change.

To strengthen your case, share redacted proposals from other properties that align with your requests. This approach can demonstrate your seriousness while fostering a cooperative dialogue with your landlord. The ultimate goal is to create a lease that reflects current market conditions and safeguards your business's long-term interests.

Step 7: Work with Experts and Finalize the Agreement

Once the lease terms are sorted out, it's time to bring in professionals to review everything and avoid potential missteps.

Work with Industrial Real Estate Specialists

Industrial real estate specialists bring valuable insights that most tenants simply can't access on their own. These experts understand the nuances of the market in the Greater Toronto Area (GTA), including the gap between asking prices and actual transaction rates. They’re also well-versed in tenant improvement allowances and vacancy rates specific to your submarket. This knowledge is essential to ensure the terms you’ve negotiated align with current market conditions.

A tenant representative can strengthen your position by touring 3–5 comparable properties and securing real proposals. This strategy creates a credible alternative, showing your landlord that you’re ready to move if the terms don’t meet your expectations. Keep in mind, landlords face significant costs when replacing tenants. These costs often include 6 to 24 months of vacancy, broker commissions ranging from 4–6% of the total lease value, and tenant improvement allowances of $20–$80 per square foot. This makes retaining tenants a priority for landlords.

The best part? Tenant representatives are typically paid by the landlord, meaning their expertise often comes at no direct cost to you. If your lease renewal exceeds $200,000 in total value, hiring a specialist is a smart move. Just make sure to begin this process 12 to 18 months before your lease expires.

Complete a Legal Review

After gathering market insights, the next step is a thorough legal review to finalise your agreement. Before signing any amendments, have a real estate lawyer go over the contract. This ensures that all negotiated terms are accurately captured and flags any clauses that could create future problems. For example, your lawyer should carefully review operating costs and Common Area Maintenance (CAM) charges to confirm there are no duplicate management fees and that capital replacement costs - like HVAC systems or roofs - are spread out over their useful life rather than charged all at once.

Environmental indemnity clauses also deserve close scrutiny. Make sure they don’t hold you responsible for contamination caused by previous tenants or third parties. Similarly, restoration obligations should only apply to improvements you’ve made, not to elements left behind by earlier tenants.

For tenants occupying over 10,000 square feet or dealing with complex CAM structures, a detailed legal review is even more critical. Your lawyer should also confirm that renewal options - such as the notice period for exercising future options and the method for calculating "market rent" - are clearly outlined.

Conclusion

Negotiating a lease renewal in the industrial real estate market is an often overlooked but valuable opportunity for tenants to cut costs and improve how their operations run. By following the seven-step process outlined here - from assessing your current lease to locking in the final agreement with expert help - you can create a clear plan to secure better terms. Starting early, ideally 18 to 24 months before your lease ends, is crucial. This timeline allows you to explore market options, consider alternative properties, and build strong leverage for negotiations. A proactive approach can lower your expenses now and give you more options in the future.

Landlords face high costs when replacing tenants, which works in your favour. Recognizing this gives you a strong edge, especially when you approach negotiations with a solid strategy.

Doing your homework on market conditions - like vacancy rates and lease trends - adds even more strength to your position. Pairing this research with professional advice ensures you’re well-prepared. Experts, whether industrial real estate consultants or legal advisers, can help you avoid costly mistakes. For example, in the 2324702 Ontario Inc. v. 1305 Dundas W Inc. case, a tenant in Ontario lost their renewal rights because they missed the written notice deadline by just two days. It’s a reminder that attention to detail, combined with expert guidance, can make all the difference.

FAQs

What if I missed my renewal notice deadline?

If you miss your renewal notice deadline, it’s important to act fast. Reach out to your landlord or property manager right away to clarify your intentions and explore any potential for an extension. Quick and clear communication can help maintain a good relationship and possibly prevent penalties or even the termination of your lease. If you’re uncertain about your options, consider speaking with a commercial real estate broker or a legal advisor who understands the regulations in the Greater Toronto Area. They can guide you in safeguarding your interests.

How do I prove fair market rent for my renewal?

To demonstrate fair market rent for your renewal, gather solid evidence of rental rates for similar properties in your area. This might include documents like recent comparable lease agreements, market rental surveys, or appraisals of similar industrial properties. Using this data helps ensure the renewal rent reflects current market conditions and can be upheld as fair market rent for comparable spaces.

Which lease costs should I cap or audit (CAM, taxes, insurance)?

When renewing a commercial lease, it's smart to pay close attention to capping or auditing costs related to CAM (Common Area Maintenance), property taxes, and insurance. For controllable CAM expenses - such as parking lot upkeep or landscaping - you can often negotiate limits on how much they can increase each year. While property taxes and insurance are usually outside your control, conducting audits can ensure you're being charged correctly and fairly. Focusing on these details can make a big difference in managing costs during lease negotiations.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist