Modular Data Centres: Investment Opportunities in GTA

Modular Data Centres: Investment Opportunities in GTA

Modular data centres (MDCs) are reshaping the data infrastructure landscape by offering scalable, pre-assembled solutions that meet the rising demand for secure and efficient facilities. The Greater Toronto Area (GTA) stands out as a prime location for these investments due to its proximity to Toronto’s financial hub, cooler climate, and supportive regulatory framework. With AI-driven workloads and data sovereignty concerns fuelling demand, the GTA’s data centre market is set to expand rapidly.

Key Highlights:

- Scalability: MDCs allow phased growth, reducing upfront costs and aligning with demand.

- GTA Advantages: Proximity to Toronto, cooler temperatures, and Ontario’s Bill 40 streamline grid connections and support job creation.

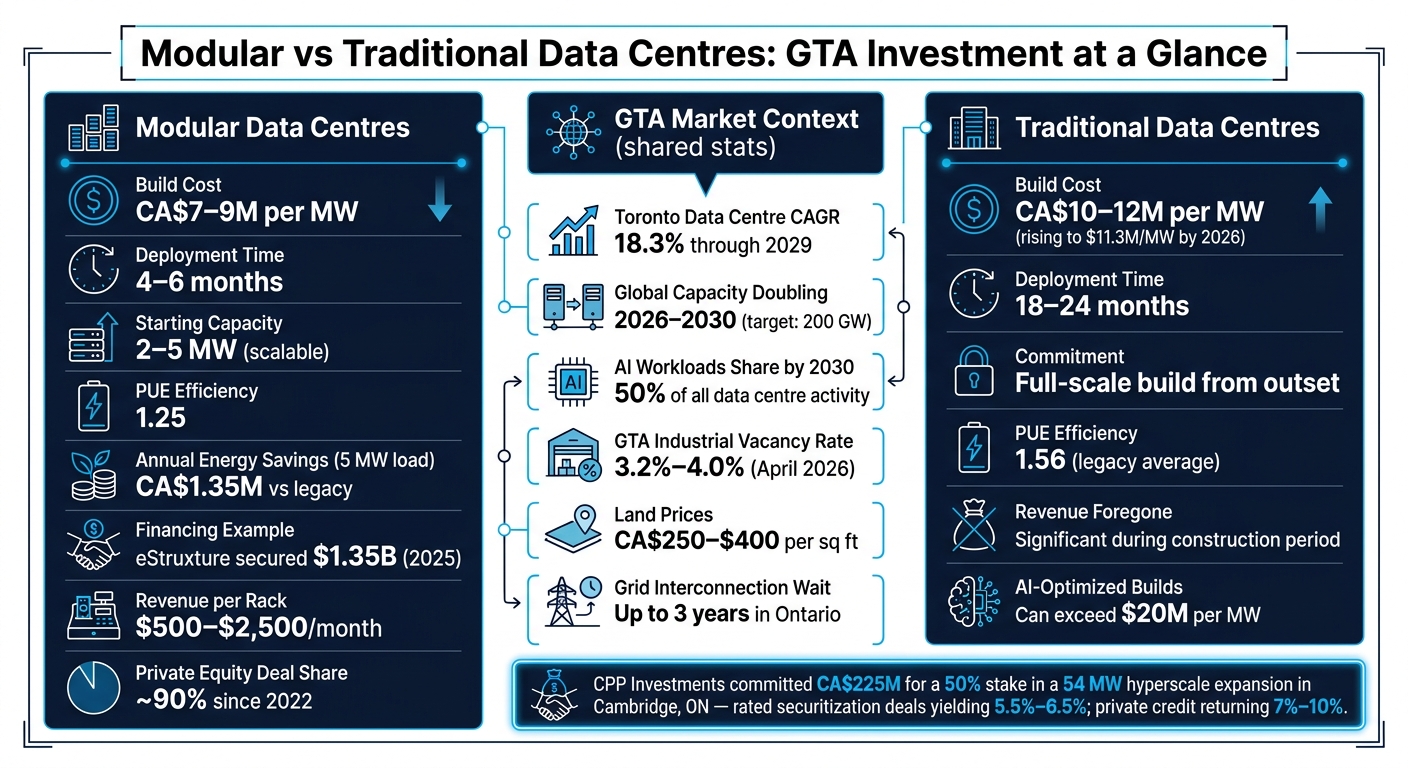

- Market Growth: Toronto’s data centre market is growing at an 18.3% CAGR through 2029, driven by AI workloads and hyperscale demand.

- Investment Benefits: Lower build costs (CA$7–9M per MW), faster deployment (4–6 months), and diversified revenue streams make MDCs attractive to investors.

For investors, securing power early, aligning with zoning requirements, and leveraging professional real estate advisory services are critical steps to tap into this growing market.

Market Demand for Modular Data Centres in the GTA

Data Centre Demand Growth in Canada

The Toronto data centre colocation market is on track to grow at an impressive compound annual growth rate (CAGR) of 18.3% through 2029, making it one of the fastest-growing markets in North America. On a global scale, data centre capacity is expected to double between 2026 and 2030, reaching a staggering 200 GW.

A major driver of this surge is AI. By 2025, AI workloads made up about 25% of all global data centre activity, and this figure is expected to hit 50% by 2030. The 2024 Fall Economic Statement highlights this trend:

"By 2030, 70 per cent of global demand for data centre infrastructure is expected to be for advanced AI workloads, with generative AI alone projected to account for 40 per cent of demand."

Recognizing this shift, the Canadian federal government has stepped in with a $700 million investment through its "AI Compute Challenge", aimed at supporting private-sector AI data centre projects. Together, these global and national trends create a strong foundation for the Greater Toronto Area's (GTA) growing data centre market.

GTA-Specific Demand Factors

Toronto already leads Canada as the largest data centre hub, but demand is outstripping supply. Absorption rates for hyperscale colocation facilities in the GTA have exceeded 100%. Ontario, home to more than 80 data centre facilities, expects 16 new centres to connect to its grid within the next decade, accounting for 13% of all new electricity demand.

The evolving nature of AI workloads is also reshaping the landscape. While AI training relies on large, centralized facilities, the shift to AI inference requires lower latency and a broader geographic spread. This shift is driving demand for distributed regional hubs, which are ideal for modular data centre deployments. As JLL explains:

"The transition from AI training to inference will redistribute workloads from centralized clusters to distributed regional hubs, fundamentally altering capacity planning and geographic deployment strategies."

Another critical factor is data sovereignty. Unlike US-based facilities, Canadian-controlled data centres are not subject to the US CLOUD Act. This makes the GTA particularly attractive for industries like financial services, healthcare, and government, where safeguarding sensitive data is a priority.

How Modular Design Meets Demand

With demand outpacing the timelines of traditional construction, modular data centres offer a practical solution. In Ontario, grid interconnection for new facilities can take up to three years, while wait times in other global markets are even longer - exceeding four years. Conventional large-scale builds simply cannot keep up.

Modular data centres, however, are delivered pre-built and pre-tested, enabling rapid deployment. This approach allows operators to roll out capacity in phases, aligning infrastructure with actual demand rather than committing to a full-scale build from the outset. It’s a more flexible and cost-effective strategy, especially given rising construction costs. Shell-and-core costs are climbing at a 7% CAGR, with projections reaching $11.3 million per MW by 2026.

For investors, modular designs offer several advantages: predictable capital deployment, reduced entitlement risk, and the ability to scale incrementally as grid capacity becomes available. In a market where power availability often outweighs location as a constraint, these benefits are increasingly important.

sbb-itb-1862e65

Site and Infrastructure Considerations

Power and Connectivity Requirements

Power availability is a major hurdle for data centre development in the Greater Toronto Area (GTA). Ontario's electricity demand is projected to grow significantly - from about 23–24 GW in 2026 to as much as 40 GW by 2050. Data centres alone are expected to account for around 13% of all new electricity demand by 2035. A key limitation is the "Flow East Towards Toronto" (FETT) interface, which restricts power transfer to approximately 5,900 MW due to 230-kV circuit constraints between Trafalgar and Richview Stations. As Bryan Gottlieb, Online Editor at Engineering News-Record, explains:

"The system operator's reliability framework identifies transmission - not generation - as the binding constraint."

To address this, Ontario's Independent Electricity System Operator (IESO) has proposed a $9.8 billion transmission upgrade plan. This includes moving towards 500-kV double-circuit lines and High-Voltage Direct Current (HVDC) links to better serve Toronto's urban core. For investors, proximity to Trafalgar and Richview Transformer Stations is a key consideration during site evaluation.

Beyond power, connectivity is equally critical. Sites need to be close to Toronto's fibre backbone and major network interconnection points to meet the low-latency demands of enterprise and hyperscale tenants. Additionally, robust backup diesel generators and specialized cooling systems are essential, which further limits the number of feasible locations.

This power and connectivity analysis lays the groundwork for evaluating zoning and land use requirements.

Zoning and Land Use

Successful data centre projects rely on secure zoning, long-term land control, and alignment with municipal infrastructure plans, as highlighted by WeirFoulds LLP.

In the GTA, data centres are typically classified as industrial or special-use under municipal zoning bylaws. Sites already zoned for industrial purposes, especially those with E1 (Employment-Industrial) or M1/M2 designations near major transmission corridors, present lower-risk opportunities. Conversely, attempting to rezone land for high-power use or backup generators can lead to delays and increase financing risks.

Municipal planning decisions are generally subject to deadlines ranging from 60 to 120 days. If a permit is denied, developers can appeal through the Ontario Land Tribunal (OLT). Under Bill 40 (Protect Ontario by Securing Affordable Energy for Generations Act, 2025), the provincial government can prioritize grid connection requests for data centres with power needs exceeding 50 MW, provided they demonstrate clear economic, strategic, or community benefits. Investors who can showcase benefits like job creation and local economic contributions are more likely to benefit from this streamlined approval process.

Land and Building Specifications

The physical footprint of a modular data centre is another critical factor, especially for future scalability. For instance, in March 2026, Prologis Canada Holding 3 GP ULC submitted a rezoning application for a two-storey, 20,438 m² data centre in Mississauga's Meadowvale Business Park. The design included 40 parking spots and three loading docks.

Key specifications for modular data centres typically include:

| Specification | Typical Requirement |

|---|---|

| Building Height | ~17 metres (2 storeys) |

| Gross Floor Area | ~20,438 m² |

| Loading Docks | 3 spaces per ~20,000 m² GFA |

| Parking | ~40 spots per ~20,000 m² GFA |

| Zoning | E1 (Employment-Industrial) or M1/M2 |

Mississauga has become a hub for data centre development due to its combination of zoning certainty, reliable power access, and proximity to fibre networks. Meeting these land and building criteria ensures modular data centres can expand efficiently as demand in the GTA continues to rise.

Twice the Density, Half the Cost: The Rise of Modular Data Centers for AI

Investment Models and Financial Considerations

Modular vs Traditional Data Centres: Cost, Speed & Scale in the GTA

Phased Capital Expenditure

Modular data centres offer a smart way to manage capital. Instead of pouring tens of millions of dollars into a project upfront, operators can start small - typically with 2 to 5 MW of capacity - and expand as needed. This "pay-as-you-grow" approach reduces the risk of holding unused assets. On average, modular builds cost around CA$7–9 million per MW, compared to CA$10–12 million per MW for traditional facilities. Plus, they can be up and running in just 4–6 months, whereas conventional builds take 18–24 months. This faster timeline means revenue starts flowing much sooner. With global construction costs expected to reach $11.3 million per MW by 2026, the cost advantages of modular builds are becoming even more compelling.

As Inflect aptly explains:

"The real TCO question is not what the facility costs to build. It is what it costs per megawatt of productive capacity, per year, over a 10-year horizon, including the revenue foregone while a traditional build is still under construction."

This phased investment strategy also paves the way for a more diversified income model.

Revenue Streams

Data centres in the GTA generate revenue from three main sources: wholesale anchor leases, retail colocation, and edge deployments. Wholesale leases, typically with hyperscale tenants, provide steady, long-term income and are the foundation for most project financing. Retail colocation, on the other hand, rents out rack space to smaller tenants and commands higher per-unit rates - ranging from $500 to $2,500 per rack per month.

AI inference workloads are also becoming a significant revenue driver. Unlike AI training, which involves periodic investments, inference delivers consistent, ongoing revenue that grows as user adoption increases. According to JLL Research, inference is expected to surpass training as the dominant workload type by 2027, shifting demand toward regional hubs - a trend that favours modular and scalable facilities in regions like the GTA.

A real-world example of successful financing in this space comes from eStruxture Data Centers. In 2025, the company secured $1.35 billion through a combination of $750 million in securitized notes and a $600 million revolving credit facility, all under a Green Finance Framework. This funding attracted pension and infrastructure funds, showcasing how diversified revenue streams and solid lease agreements can unlock large-scale institutional financing.

Risk and Return Analysis

While the GTA data centre market offers great potential, it’s not without challenges. Key risks include high power costs, delays in grid connections, and evolving AI infrastructure needs. For instance, connecting to Ontario's grid can take three years or more in major markets, making early engagement with the Independent Electricity System Operator (IESO) essential.

Modular designs help address some of these risks. By scaling incrementally, operators avoid overbuilding, and the energy savings can be substantial. For example, a modular facility with a PUE of 1.25 can save about CA$1.35 million annually for a 5 MW load compared to a legacy facility with a PUE of 1.56. However, AI-optimized sites with advanced cooling systems and high-density racks can push costs above $20 million per MW, so early design decisions have long-term financial implications.

On the return side, private equity has dominated the data centre market, accounting for nearly 90% of deal activity since 2022. Canadian pension funds are also increasingly viewing data centres as core infrastructure. For example, CPP Investments committed $225 million for a 50% stake in a 54 MW hyperscale expansion in Cambridge, Ontario. This joint venture included Related Digital, TowerBrook Capital Partners, and Ascent. Rated securitization deals are yielding 5.5% to 6.5%, while private credit opportunities offer returns of 7% to 10%. For investors who secure power early and structure leases effectively, the GTA modular data centre market presents an attractive risk-adjusted return opportunity.

The Role of Industrial Real Estate Advisory

Navigating Complex Real Estate Transactions

Finding the right site for a modular data centre is a far cry from your typical industrial property deal. Here, power capacity takes precedence over square footage. Smaller modular and edge units often need between 5–10 MW, while hyperscale facilities can demand upwards of 100 MW. As Andy Cvengros, Managing Director at JLL, explains:

"It is vital to have an agreement with the utility to supply your site with power. Just because the infrastructure is there doesn't mean the utility can provide it."

But power isn’t the only consideration. Investors must also navigate Greater Toronto Area (GTA) zoning bylaws, which classify data centres as industrial or special-use properties. These bylaws impose restrictions on factors like noise, setbacks, and traffic - all of which can directly affect site design. Adding to the complexity, municipal approval timelines in the GTA can stretch to 24–36 months. This makes early and thorough due diligence critical, as certain locational risks might disqualify a site altogether. Advisory services play a key role in simplifying this intricate process, ensuring investments stay on track.

How Lennard Commercial Adds Value

To tackle these challenges, Michael Law of Lennard Commercial offers deep market expertise, helping investors navigate the GTA’s competitive data centre landscape. With GTA industrial vacancy rates ranging from 3.2% to 4.0% (as of April 2026) and land prices between CA$250–400 per square foot, Lennard Commercial’s ability to identify off-market opportunities is a significant advantage.

The firm oversees a comprehensive 30–75-day due diligence process, coordinating environmental assessments, structural inspections, and utility verifications. They also keep an eye on pending bylaw amendments that could impact project timelines or feasibility. This expertise is particularly valuable for investors exploring adaptive reuse of older industrial buildings. As Peter Skae, Managing Director of Data Center Technical Services at JLL, points out:

"The power infrastructure on such a site is more valuable than the data centre itself."

By offering this tailored guidance, Lennard Commercial helps investors tap into the GTA’s growing modular data centre market with confidence and precision.

Specialized Industrial Property Services

Lennard Commercial’s services are designed to support every stage of a modular data centre investment, ensuring projects are executed efficiently and in compliance with local regulations. When it comes to site acquisition, the firm provides a range of services, including property valuation, transaction coordination, and lease structuring. Their expertise in lease renewals and term negotiations, paired with landlord representation, ensures favourable outcomes for clients.

The firm also helps investors navigate Ontario’s shifting regulatory landscape. For example, they assist with compliance under the Industrial Green Development Standard Tier 1, which became mandatory for new GTA developments in March 2025. Additionally, Ontario’s Bill 40 (Protect Ontario by Securing Affordable Energy for Generations Act, 2025) prioritizes grid access for data centres that demonstrate clear economic and strategic benefits. Having an advisor who understands both the real estate and regulatory aspects ensures seamless project progression - from site selection to full market integration. This expertise is a game-changer for investors aiming to make a lasting impact in the modular data centre space.

Conclusion: Modular Data Centres in the GTA

Scalability and Market Outlook

The modular data centre market in the Greater Toronto Area (GTA) is poised for steady growth. Globally, the data centre industry is projected to expand significantly, with the Americas expected to grow at a 17% compound annual growth rate (CAGR) through 2030. This surge in capacity - 100 GW of new global additions - is estimated to generate CA$1.2 trillion in real estate asset value.

In the GTA, the rise of AI-driven workloads is transforming capacity planning and deployment strategies. By 2027, inference workloads are anticipated to surpass training as the primary AI demand, leading to increased focus on distributed regional hubs. Modular designs are particularly suited to meet this need. One example is Yondr's 27 MW Toronto campus, which became operational in April 2026. Highlighting this trend, John Madden, Chief Data Centre Officer at Yondr, remarked:

"Demand for capacity is accelerating at a pace we've never experienced before, driven by AI scale and a shift toward compute-led economies."

Canada's emphasis on data sovereignty further strengthens the GTA's position. Facilities under exclusive Canadian control are exempt from the US CLOUD Act, making the GTA an attractive hub for government, financial, and enterprise data. This advantage will continue to shape the appeal of modular data centre designs in the region.

Key Takeaways for Investors

Several factors make modular data centres in the GTA a compelling investment opportunity, centred around power access, phased scalability, and regulatory alignment. Securing power early - whether through utility agreements, behind-the-meter solutions, or battery storage - is crucial, as grid interconnections in Ontario can take up to three years. Phased modular development mitigates entitlement risks and provides greater financing predictability. Additionally, Ontario's Bill 40 offers regulatory support for facilities exceeding 50 MW, particularly those serving provincial economic priorities.

Investors can leverage these opportunities by focusing on the strengths outlined above. For those navigating the competitive GTA market, Lennard Commercial offers expertise in identifying powered, industrially zoned land and managing the due diligence process, from environmental assessments to utility verification and lease structuring. With the right approach, modular data centres in the GTA promise both financial and operational rewards.

FAQs

How do I secure power for a modular data centre site in the GTA?

When setting up a modular data centre in the Greater Toronto Area, ensuring a reliable power supply is a critical step. Start by selecting a location early in the planning process. Look for sites near high-capacity power infrastructure, such as transmission corridors or industrial zones, as these areas are better equipped to handle the energy demands of a data centre.

Next, prepare and submit a detailed service request to the local utility provider. This request should include comprehensive site plans and precise load calculations to help the provider assess your power needs accurately. For larger-scale projects, you may need to incorporate on-site solutions like transformers or substations to meet the facility's energy requirements.

Finally, keep an eye on regional grid expansions and upgrades. Staying informed about these developments can help you anticipate and secure the necessary power capacity, ensuring your data centre operates without interruptions.

Which GTA municipalities and zoning types are best for data centres?

Mississauga stands out as a prime location for data centres, especially in industrial hubs like Meadowvale Business Park. These areas are close to major transmission infrastructure and benefit from zoning regulations that support such developments. With rezoning applications for data centres currently under review, these locations offer strong potential for investment opportunities.

What lease structure is ideal for modular data centre investments?

A long-term anchor lease supported by hyperscale tenants is often the preferred choice when financing modular data centres. In contrast, for more traditional ownership models, stabilized multi-tenant leases - complete with detailed service-level agreements - are typically the standard approach.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist