Checklist for Structuring Sale-Leaseback Deals

Checklist for Structuring Sale-Leaseback Deals

A sale-leaseback allows businesses to sell their property while continuing to use it as tenants, unlocking 100% of the property's equity. This approach is especially popular in the Greater Toronto Area for industrial properties, where demand is high, and financing costs are rising. By selling their property and leasing it back, companies can free up capital to invest in core operations.

Key points to consider:

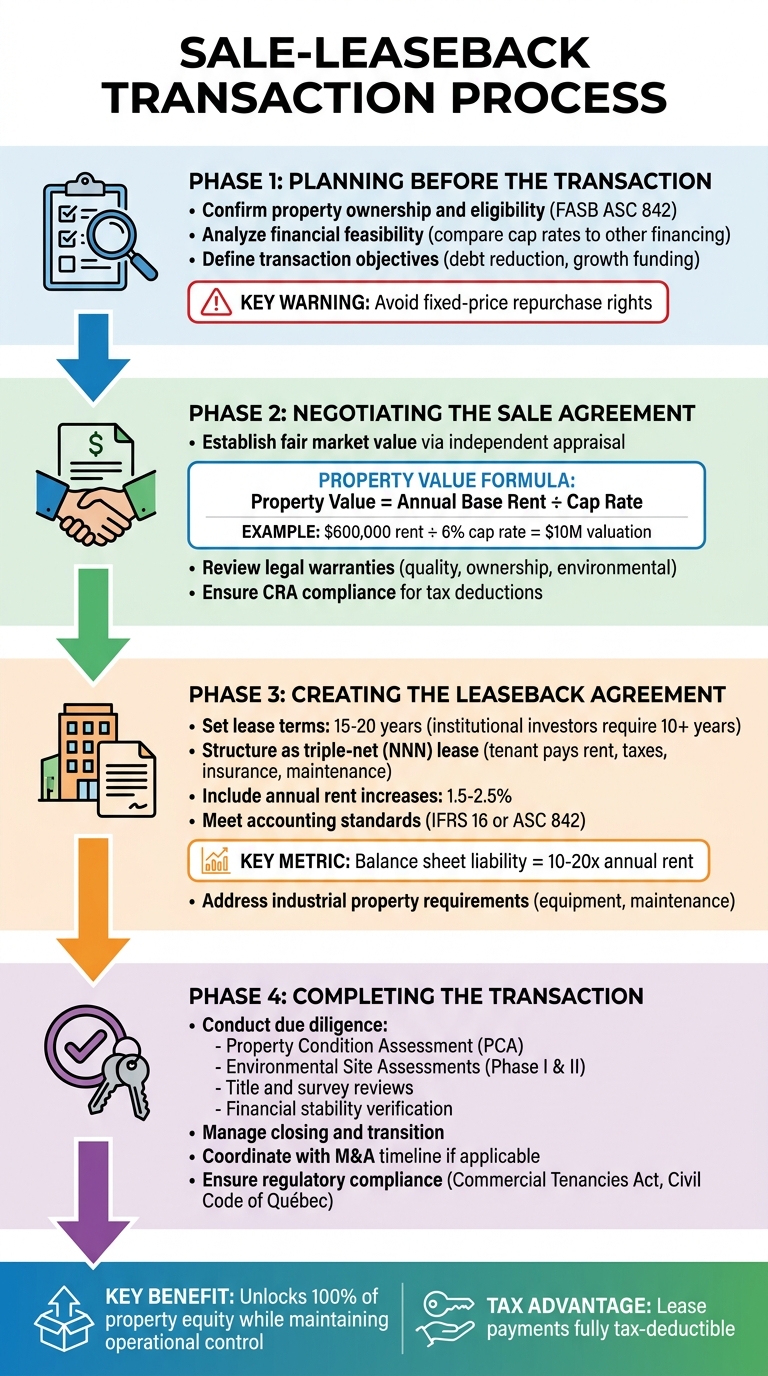

- Eligibility: Ensure the property qualifies as a sale under FASB ASC 842. Avoid fixed-price repurchase rights that could reclassify the deal as financing.

- Valuation: Use the formula: Annual Rent ÷ Cap Rate = Property Value. For example, $600,000 rent at a 6% cap rate equals a $10M valuation.

- Lease Terms: Most agreements are 15–20 years, often triple-net (NNN), where tenants cover rent, taxes, insurance, and maintenance.

- Financial Feasibility: Compare cap rates to other financing options. Lease payments are tax-deductible but may create long-term liabilities.

- Legal and Tax Considerations: Address warranties, environmental liabilities, and ensure lease payments align with CRA guidelines.

- Due Diligence: Conduct thorough property and financial reviews, including environmental assessments and structural inspections.

A well-structured sale-leaseback can provide immediate liquidity and improve financial flexibility. However, missteps in structuring or aligning terms with business goals can lead to long-term challenges. Expert advice is crucial to navigate the process effectively.

Sale-Leaseback Transaction Process: 4-Phase Checklist for Structuring Deals

Planning Before the Transaction

Confirming Property Ownership and Eligibility

Before moving forward, make sure your property qualifies as a legitimate "sale" under the guidelines of FASB ASC 842. According to these standards, a valid sale requires a written agreement where the seller transfers both legal title and control to the buyer. Jo Claire Spear of Trenam explains:

"The transaction needs to first qualify as a 'sale.' Ideally, there should be: (a) the existence of a written sales contract with a seller who holds legal title and control over the property, with (b) a transfer of title and control to the buyer upon exchange of consideration".

Be cautious about potential disqualifiers. If the agreement includes a fixed-price repurchase right or the property is so specialized that it limits alternate uses, the transaction could be classified as a financing arrangement instead of a sale. Alex Lubyansky, Managing Partner at Acquisition Stars, warns:

"If the seller-lessee retains a repurchase right at a fixed price, a right of first refusal at fair value, or any other arrangement that might prevent the transfer of control, the transaction may fail sale recognition and instead be accounted for as a financing".

It's also important to verify that the lease terms align with the legal warranties of ownership stated in the purchase offer.

Analyzing Financial Feasibility

Understand your capital costs before committing to the transaction. The capitalization rate (cap rate) in a sale-leaseback essentially reflects your financing cost. Compare this rate to other options like traditional debt or equity issuance. If debt financing offers a lower interest rate or equity issuance reduces financial strain, those alternatives might be more appealing.

Run detailed lease models to account for variables like lease duration, rental rates, and escalation clauses (e.g., annual increases of 2% or a 10% bump every five years). Don’t overlook tax considerations: while selling the property eliminates depreciation benefits, lease payments become fully tax-deductible as rental expenses. For properties with specialized equipment, outline maintenance responsibilities clearly to avoid unexpected costs.

This financial groundwork is essential for setting clear transaction goals.

Defining Transaction Objectives

Once you've thoroughly analyzed your property and financial situation, define the purpose of the transaction and ensure it aligns with your broader business strategy. Are you aiming to reduce debt, fund growth, or improve financial metrics? If the deal is poorly structured, it could leave your business with burdensome lease obligations or accounting complications.

Think carefully about lease terms, especially for commitments spanning 15 to 20 years. Institutional investors often require lease terms of at least 10 years, with specialized facilities sometimes needing commitments of up to 25 years. Keep in mind that under FASB ASC 842, a long-term triple-net lease can create a balance sheet liability equivalent to 10 to 20 times your annual rent. Engage advisors early to assess impacts on leverage and covenants.

sbb-itb-1862e65

Negotiating the Sale Agreement

Establishing Fair Market Value

Getting the valuation right is crucial. The sale price must align with fair market value to meet both accounting standards and regulatory requirements. To achieve this, start with an independent professional appraisal. This ensures your valuation is objective and grounded in reliable data. Stan Prokop, Founder of 7 Park Avenue Financial, highlights the importance of this step:

"Asset valuation is critical in any sale leaseback transaction. Independent appraisals protect both the borrower and the lender".

An appraisal should consider key real estate factors like location, asset class, and local market trends. For industrial properties, it’s essential to evaluate the asset’s age, its remaining useful life, and how integral it is to your operations. Another critical factor is the tenant’s creditworthiness - stronger credit often translates to lower capitalization rates, which can boost the sale price. Avoid inflating the sale price by agreeing to above-market rent. While this might seem appealing short term, it can hurt your profitability and make the property harder for investors to lease out later.

The property’s value hinges on its capitalization rate, calculated using this formula: Property Value = Annual Base Rent ÷ Cap Rate. To secure a better cap rate, consider engaging an advisor to run a competitive bidding process, which could improve your rate by 50 to 100 basis points.

Once you have a reliable valuation, the next step is to dive into the legal and tax aspects of the agreement.

Reviewing Legal and Tax Requirements

Property sales in Canada come with specific legal obligations that directly influence your sale agreement. For example, under the Civil Code of Québec, the legal warranty of quality ensures the property is free of hidden defects at the time of sale. If you provide this warranty, your leaseback agreement must clearly state that you, as the tenant, are responsible for addressing any defects existing at the time of closing. The legal warranty of ownership also requires that the property is free of undisclosed rights and complies with environmental legislation.

Environmental liability is particularly important. If you warrant that the property is uncontaminated at closing, your lease must explicitly confirm that you remain responsible for any pre-existing contamination, regardless of its origin. Gowling WLG underscores this point:

"The lease between the parties must be carefully tailored to the transaction, and the terms and conditions of this lease must be consistent with the provisions of the offer to purchase notably those provisions of the offer relating to the seller's conventional representations and warranties and the legal warranties of quality and ownership".

For industrial properties, it’s also essential to clarify the status of specialized equipment. Decide whether this equipment is part of the sale or remains your property, as this affects both maintenance responsibilities and end-of-lease removal obligations.

On the tax side, ensure your lease payments qualify as fully deductible business expenses under CRA guidelines. Additionally, under IFRS 16, your gain on the sale is often capped based on the residual interest in the asset.

Creating the Leaseback Agreement

Setting Lease Terms and Rent Payments

The leaseback agreement lays out how long you'll remain in the property and clarifies your payment responsibilities. Typically, institutional investors prefer initial lease terms of at least 10 years, with some specialised facilities requiring commitments of 15 to 25 years. To keep your options open after the initial term, negotiate multiple renewal periods - usually two or three terms spanning 5 to 10 years each.

Rent payments in these agreements are often structured as triple-net (NNN) leases. Under this arrangement, you, as the tenant, take on property taxes, insurance, and maintenance costs, which ensures steady income for the investor. Annual rent increases, usually between 1.5% and 2.5%, are either fixed or tied to the Consumer Price Index. For instance, if your annual rent is C$600,000 and the investor's cap rate is 6%, the implied purchase price of the property would be C$10,000,000. You might also want to include a Right of First Offer (ROFO) or Right of First Refusal (ROFR) in the lease, giving you the opportunity to buy back the property in the future.

Once you've defined the lease terms and rent structure, the next step is ensuring these align with current accounting rules.

Meeting Accounting Standards

To qualify as an operating lease under accounting standards, the agreement must be structured carefully. In Canada, public entities follow IFRS 16, which requires the buyer-lessor to gain control of the asset for the transaction to qualify as a sale. If the leaseback is classified as a finance lease, control is not considered transferred. Sensiba explains:

"The buyer-lessor is not considered to have control of the asset if the leaseback would be classified as a finance lease or a sales-type lease."

If you include a repurchase option, it should be structured at fair market value. Fixed-price repurchase rights can prevent the transaction from being recognised as a sale, resulting in it being treated as financing instead. To avoid this, ensure any repurchase option reflects the fair market value at the time of exercise, and confirm that similar assets are readily available on the market.

For cross-border transactions or private equity deals governed by ASC 842, you'll need to recognise a right-of-use asset and a lease liability on your balance sheet. This liability is calculated as the present value of future lease payments. For long-term triple-net leases on industrial properties, this liability can be 10 to 20 times your annual rent. Additionally, sale prices and lease payments must align with fair market value. If the sale price exceeds market value, the excess may be treated as prepaid rent; if it's below market value, it could be recorded as additional financing. Proper structuring ensures compliance and accurate financial reporting, supporting the financial analysis conducted earlier in the process.

Accommodating Industrial Property Requirements

Once the financial and accounting aspects are sorted, it’s important to address the specific needs of industrial properties. The lease should clearly define who is responsible for specialised equipment like overhead cranes, loading docks, or HVAC systems. This includes outlining maintenance duties and removal obligations at the end of the lease term.

For structural components, such as roofs, foundations, and building systems, the triple-net lease typically makes the tenant responsible for all repairs and capital expenses. To protect your operations, include landlord cooperation clauses. These provisions ensure the landlord assists with zoning changes, building permits, and compliance with environmental regulations. This is especially crucial for industrial facilities that may need modifications to adapt to changing manufacturing or logistics requirements. Gowling WLG highlights this:

"The lease becomes a key asset, protecting the seller-tenant's rights to remain in the building and to continue operating its business therein and therefrom while ensuring the buyer-landlord a certain return on investment through rent."

If your seller warranties included environmental representations, make sure the lease specifies that you remain responsible for any pre-existing contamination, even if discovered later. These provisions help ensure the transaction aligns with the strategic goals set during the negotiation phase, preserving operational continuity while meeting investor expectations.

Completing the Sale-Leaseback Transaction

Conducting Due Diligence and Managing Risks

Thorough due diligence is critical to uncover potential risks. The buyer-lessor will carefully review financial metrics to confirm your ability to meet long-term lease obligations. They’ll also conduct searches for bankruptcy filings, judgments, tax liens, and litigation to identify liabilities that could affect your stability.

For the property itself, due diligence includes title and survey reviews to flag any easements or encroachments, checks for zoning code compliance, and Property Condition Assessments (PCA) to evaluate structural and mechanical systems. The PCA helps identify upcoming capital expenditures, which typically become your responsibility under a triple-net (NNN) lease structure. Additionally, Environmental Site Assessments (Phase I and Phase II ESAs) are essential to detect contamination, as any undiscovered issues can become your liability under NNN terms.

Gowling WLG highlights the importance of aligning lease terms with the transaction:

"The lease between the parties must be carefully tailored to the transaction, and the terms and conditions of this lease must be consistent with the provisions of the offer to purchase."

This alignment ensures you remain accountable for pre-existing conditions, as agreed, minimizing the risk of disputes after closing.

Managing Closing and Transition

After completing due diligence, focus on managing the closing process for a smooth transition. This step becomes particularly complex if the sale-leaseback is tied to a larger M&A transaction. Alex Lubyansky, M&A Attorney at Acquisition Stars, explains:

"The sale-leaseback introduces a third party (the property investor) into the M&A timeline. Coordinating the real estate close with the business close requires parallel diligence tracks and careful sequencing of conditions precedent."

In simultaneous transactions, the M&A purchase agreement and real estate sale agreement should be interdependent, ensuring one cannot proceed if the other fails.

To streamline the process, create a detailed closing agenda to track critical dates and prepare all necessary documents. Secure corporate approvals and ensure compliance with relevant laws. In Ontario, this means adhering to the Commercial Tenancies Act, while Quebec transactions must follow the Civil Code of Québec. For properties in the Greater Toronto Area, provide proof of compliance with Green Development Standards for new builds or major renovations. The Statement of Adjustments will finalize prorated property taxes, utilities, and rent, ensuring a clean and organized handover on the closing date.

What is a Sale / Leaseback? [Commercial & Industrial Real Estate]

Conclusion

A sale-leaseback can transform real estate into immediate capital while allowing businesses to maintain operational control. By unlocking 100% of a property's market value, this approach turns an illiquid asset into working capital through long-term lease agreements. When executed effectively, it not only provides a financial boost but also enhances a company's overall financial health.

This strategy offers tax advantages and improves financial ratios. Lease payments are often fully tax-deductible as operating expenses, and the freed-up capital can improve key metrics. As Bronwyn Scrivens points out:

"The sale leaseback provides an opportunity for a win-win transaction between the owner/operator and investor, where all parties share involvement in the framework of a deal that meets their goals".

However, these transactions require careful execution. From aligning the lease terms with the purchase agreement to complying with legal frameworks like Ontario's Commercial Tenancies Act or Québec's Civil Code, every detail matters. Alex Lubyansky, M&A Attorney at Acquisition Stars, cautions:

"Done incorrectly, it creates lease obligations the business cannot service, accounting complications that move lenders, and tax exposure neither side planned for".

In Toronto's competitive industrial real estate market, partnering with experienced advisors, such as Lennard Commercial - Industrial Real Estate Services, ensures a tailored approach that aligns with both financial and operational objectives.

With industrial properties in high demand and financing conditions constantly evolving, sale-leasebacks present a smart alternative for businesses seeking immediate liquidity without compromising long-term stability.

FAQs

Will my sale-leaseback qualify as a true “sale” under ASC 842 or IFRS 16?

A sale-leaseback is considered a genuine "sale" under ASC 842 or IFRS 16 only if control of the asset is transferred to the buyer-lessor. This determination hinges on specific criteria, including the IFRS 15 transfer test and other control-related factors. If control does not pass to the buyer-lessor, the transaction is instead classified as a financing arrangement rather than a sale.

How do I know if the cap rate makes this cheaper than borrowing?

When deciding if a sale-leaseback deal is more cost-effective than borrowing, start by comparing the cap rate to your company’s borrowing rate. If the cap rate results in rent payments that are lower than what you'd pay on a loan, it could be a smart financial move. Additionally, a lower cap rate can free up more capital, making the sale-leaseback arrangement an attractive option for your business.

What risks do I keep under a triple-net (NNN) industrial leaseback?

Under a triple-net (NNN) industrial leaseback, tenants take on several critical financial responsibilities: property taxes, insurance, and maintenance costs. These obligations can become substantial, particularly if property taxes rise or if tax assessments are disputed.

It's also vital for tenants to carefully examine escalation clauses, common area maintenance (CAM) charges, and environmental indemnities to gauge their full financial exposure. To manage these risks, negotiating favourable lease terms and implementing sound risk management strategies can make a significant difference.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist