Supply Chain Disruptions: GTA Warehouse Demand

Supply Chain Disruptions: GTA Warehouse Demand

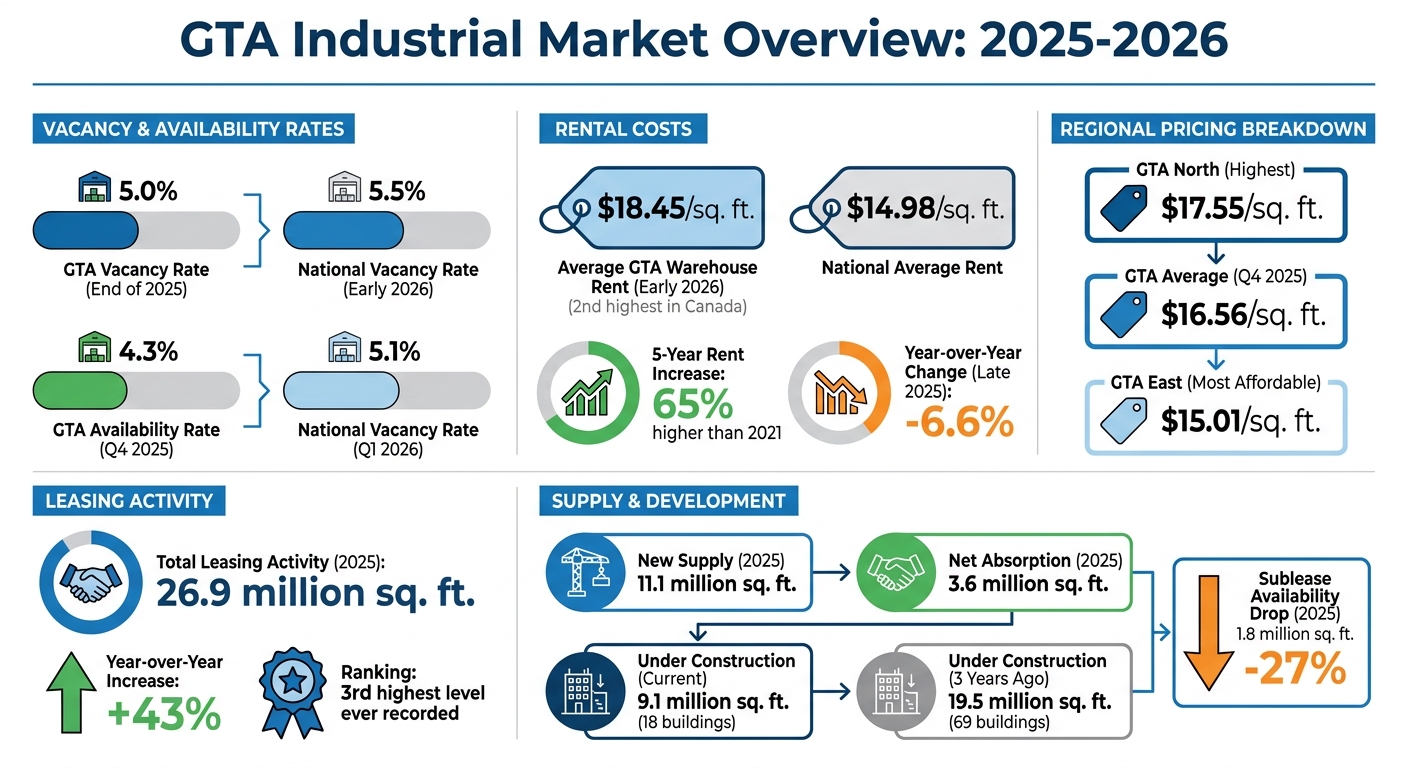

The Greater Toronto Area (GTA) is grappling with a surge in warehouse demand, driven by supply chain uncertainties and shifting inventory strategies. In 2025, leasing activity rose by 43%, totalling 26.9 million square feet. Businesses are moving away from just-in-time models, opting instead for safety stock approaches that require more storage space. This has tightened the market, with vacancy rates at 5.0% by the end of 2025 and rents reaching $18.45 per square foot in early 2026 - 65% higher than five years ago. Developers are scaling back speculative projects, focusing on tenant-specific builds due to high land costs and fluctuating material prices.

Key points:

- GTA industrial vacancy rate: 5.0% (2025), compared to 5.5% nationally (2026).

- Average warehouse rent: $18.45/sq. ft., with GTA North being the most expensive ($17.55/sq. ft.) and GTA East the most affordable ($15.01/sq. ft.).

- Sublease availability dropped by 27% in 2025, further limiting options.

- E-commerce and trade risks are reshaping the role of warehouses, making them critical for inventory and tariff management.

The market is expected to stabilize by late 2026 as trade uncertainties ease, creating opportunities for businesses to negotiate better terms or secure space in less costly submarkets. Companies must act strategically to navigate these trends and secure their operational needs in a competitive landscape.

GTA Industrial Market Overview

GTA Warehouse Market Statistics 2025-2026: Vacancy Rates, Rental Costs and Supply Data

The GTA industrial market started 2026 in a period of adjustment, with vacancy rates beginning to ease as businesses recalibrate to evolving pricing and supply realities. Even with this shift, the region's market remains much tighter than the national average. These trends highlight how supply chain challenges continue to drive demand.

Vacancy Rates and Supply

By the end of 2025, the GTA's vacancy rate stood at 5.0%, outperforming the national average of 5.5% recorded in early 2026. This reflects the GTA's role as a key logistics hub. In 2025, 11.1 million square feet of new supply entered the market, alongside a net absorption of 3.6 million square feet. However, the pipeline of projects under construction dropped to just 9.1 million square feet across 18 buildings, a sharp decline from the 19.5 million square feet spread over 69 buildings just three years earlier.

Developers are grappling with several challenges, including high land costs tied to purchases made at peak market conditions, fluctuating material and labour prices, and persistent trade tensions. These pressures have shifted the focus toward design-build projects for committed tenants, moving away from speculative developments.

Sublease availability also tightened significantly in 2025, dropping 27% (or 1.8 million square feet). Many businesses are holding onto their existing spaces, further limiting available inventory.

Rental Costs and Pricing

Warehouse rents in the GTA climbed to $18.45 per square foot in early 2026, making it the second-highest rate in Canada and well above the national average of $14.98 per square foot. Although rents eased by 6.6% year-over-year by late 2025, they remain 65% higher than they were five years ago.

The region also shows distinct pricing differences. GTA North commands the highest average net rents at $17.55 per square foot, whereas GTA East offers the most affordable rates at $15.01 per square foot. These variations are influenced by proximity to major transportation routes and urban centres, with businesses carefully balancing accessibility and cost.

These regional dynamics reflect broader market trends. Keith Reading, Senior Director of Research at Morguard, shared his outlook on future conditions:

"But if we do see some sort of agreement on trade and trade stability, I think businesses will know what the environment's going to be like, and they can dust off those expansion plans, and we could see economic activity and growth increase toward the end of 2026".

These pricing and vacancy trends set the stage for a deeper look at how supply chain disruptions are reshaping the market.

sbb-itb-1862e65

Supply Chain Disruptions Driving Warehouse Demand

The shift from just-in-time inventory models to safety stock strategies is reshaping warehouse demand in the Greater Toronto Area (GTA). Companies are now focused on securing additional storage capacity to navigate ongoing supply chain disruptions.

Post-Pandemic Supply Chain Changes

The pandemic has forced businesses to rethink their logistics strategies, with reliability now taking precedence over cost. This has led to a growing emphasis on nearshoring and reshoring, with companies favouring manufacturing and distribution networks closer to home. The GTA's well-connected highway system, proximity to Pearson International Airport, and access to rail and port facilities make it a key player in these revamped supply chains.

Warehouses are no longer just storage spaces; they’ve become vital tools for managing trade risks. For example, some companies are modifying imported goods - like food products - within Canadian warehouses to meet the requirements for USMCA exemptions. This allows them to ship goods to the United States without incurring tariffs.

Reduced New Supply

New warehouse construction in the GTA has slowed significantly. Developers are pulling back on speculative projects due to soaring land costs from peak market purchases, unpredictable material and labour expenses, and potential tariff impacts. Instead, the focus has shifted to design-build projects tailored for specific tenants.

Adding to the challenge, sublet space availability dropped by 27% (or 1.8 million square feet) in 2025, as businesses opted to hold onto their existing facilities. This tightening of supply underscores the growing need for more adaptable fulfillment solutions.

E-Commerce and Last-Mile Delivery

E-commerce and logistics remain key drivers of industrial real estate demand in the GTA. Retailers and shippers are increasingly relying on third-party logistics (3PL) providers to handle e-commerce fulfillment. This approach offers flexibility in uncertain economic times, as explained by Juana Ross, Research Manager at Cushman & Wakefield:

"They would rather avoid a long-term lease obligation at these very high rates and prioritize the flexibility of 3PLs more so than the flexibility of having their space themselves".

Modern e-commerce operations demand facilities with over 32-foot clear heights to accommodate mezzanines and automated storage systems. Additionally, easy access to public transit is becoming essential to attract the workforce needed for labour-intensive tasks like picking and packing.

Market Data and Forecasts for 2025-2026

The Greater Toronto Area (GTA) industrial market demonstrated resilience in Q4 2025, recording a net absorption of 4.2 million square feet. For the entire year, absorption reached 3.6 million square feet, reflecting the sector's ability to weather economic challenges. Across Canada, industrial assets remain a preferred choice for lenders and investors, with early signs of recovery being noted.

Absorption and Development Activity

Leasing activity in 2025 hit 26.9 million square feet, marking a 43% increase and achieving the third-highest level ever recorded. However, speculative development slowed significantly. Currently, only 18 buildings totalling 9.1 million square feet are under construction, a sharp drop compared to three years ago, when 69 buildings amounting to 19.5 million square feet were in progress. This reduction is likely to persist into 2026 as developers face challenges such as elevated land costs, fluctuating material prices, and potential tariffs. Experts suggest that economic activity may pick up towards late 2026, provided trade becomes more stable and businesses resume expansion plans.

These trends provide an opportunity to contrast the GTA's performance with national market data.

GTA vs. National Market Comparison

The GTA market continues to outpace national averages in several key metrics, supported by strong absorption numbers. By Q4 2025, the GTA's vacancy rate fell to 4.1%, while the availability rate stood at 4.3%, reflecting a 40-basis-point drop compared to the previous year. Rental rates averaged $16.56 per square foot, a 6.6% decrease from the prior year, though still 65% higher than five years ago. Nationally, the vacancy rate declined to 5.1% in Q1 2026, marking its first improvement since 2022.

| Metric | Greater Toronto Area (GTA) | National (Canada) |

|---|---|---|

| Vacancy/Availability Rate | 4.1% (vacancy) / 4.3% (availability) (Q4 2025) | 5.1% (Q1 2026) |

| Net Rental Change (Y-o-Y) | -6.6% (easing from peaks) | Incremental recovery expected |

| New Supply Volume | 9.1 million sq. ft. (under construction) | Declining speculative pipeline |

| Leasing Activity | 26.9 million sq. ft. | Surged in H2 2025 |

Market conditions are expected to stabilize by late 2026, driven by clearer trade policies and improved financing environments.

Industry-Specific Warehouse Demand in the GTA

The GTA's warehouse market reflects broader trends while also highlighting how industry-specific factors are shaping demand. Supply chain uncertainties continue to push businesses toward targeted warehouse solutions.

3PL Providers and Manufacturing

In 2025, third-party logistics (3PL) providers led leasing activity in the GTA as companies sought flexibility in response to high rental costs and economic instability. Manufacturers are also adapting, using GTA warehouses to mitigate trade risks and navigate tariff challenges.

For instance, in April 2026, Lisa McEwan, co-owner of Hemisphere Freight, shared an example of a client importing chocolate from Europe to a Canadian warehouse. The product is then processed into a new food item, making it compliant with the USMCA, and shipped to the U.S. tariff-free. This strategy, often referred to as "trade contortion", has turned warehouses into active centres for production and processing. Alan Dewar, Executive Vice-President at GHY International, summed it up well:

"Warehouse demand isn't being driven by growth – it's being driven by uncertainty. Warehouses aren't just storage anymore; they're a front-line tool for managing trade risk".

This shift isn't limited to massive operations. Smaller facilities are also becoming essential players in the market.

Small-to-Mid Bay Warehouse Spaces

Smaller warehouse spaces are playing a crucial role as businesses navigate ongoing trade uncertainties. In 2025, properties under 50,000 square feet accounted for 81.1% of all industrial transactions in the GTA. Kristina Bowman, National Research Manager at Cushman & Wakefield, emphasized this trend:

"The real demand really continues to be in that sub-25,000-square-foot space".

Flex industrial buildings, which combine warehouse, office, and showroom functions, are particularly attractive. They allow businesses to streamline operations by consolidating multiple functions into one location.

Lease Expirations and Renewals

Lease expirations are creating opportunities for negotiation, especially in high-demand areas like Mississauga and Brampton. By Q1 2026, availability in these hubs reached 6.1%. Notably, about 33% of the available space in the West GTA consists of high-quality sublease options in buildings less than five years old. Many of these spaces feature modern 36-foot-plus clear heights, ideal for advanced automation.

For tenants facing lease renewals, this surplus of sublease inventory offers a chance to secure better deals. Landlords, eager to fill these spaces, are more likely to offer competitive pricing, flexible lease terms, and tenant improvement allowances. These dynamics reflect the tight supply and growing demand for adaptable warehouse solutions.

Approaches for Managing GTA Warehouse Market Conditions

Expected Market Stabilization by Mid-2026

The GTA warehouse market is showing signs of moving toward stability. Recent trends highlight a tightening market, indicating that excess inventory is being absorbed and the sector is heading toward balance.

Experts suggest that trade stability expected in late 2026 could pave the way for renewed growth, urging businesses to act sooner rather than later. Preparing now is crucial. Companies that assess their operational needs and explore submarket options today will be better positioned to respond when conditions improve. With vacancy rates sitting at 4.3% in Q4 2025, landlords continue to hold the upper hand, but increased trade certainty could shift the balance, potentially leading to more favourable lease terms by the end of 2026.

These shifting market trends highlight the importance of specialized guidance to navigate the opportunities ahead.

Customized Industrial Real Estate Services

In this evolving market, having access to tailored real estate expertise is more critical than ever. Standard property searches often fail to address the specific challenges businesses face in the GTA's tight warehouse market. That’s where Lennard Commercial - Industrial Real Estate Services steps in with data-driven strategies designed to meet these unique demands. Whether you're negotiating a lease renewal in Mississauga, relocating to a more cost-effective area like GTA East (where rates average $15.01 per square foot versus $17.55 in GTA North), or considering 3PL integration to avoid long-term commitments at peak pricing, their expertise uncovers overlooked opportunities.

The firm’s services go beyond traditional leasing. From finding warehouse space that meets USMCA compliance for tariff circumvention to sourcing modern Class A facilities with 32-foot clear heights, Michael Law of Lennard Commercial delivers customized solutions backed by exclusive market insights. This approach helps businesses secure the right spaces despite limited availability, negotiate better terms during lease renewals, and adapt their operations to manage ongoing trade challenges.

For more details, visit Lennard Commercial - Industrial Real Estate Services.

Conclusion

The GTA industrial market is undergoing a transformation, largely influenced by ongoing supply chain uncertainties. Warehousing has shifted from being just about storage to becoming a key element in managing risks tied to supply chain disruptions, trade challenges, and infrastructure strains. Leasing activity jumped by 43% in 2025, while availability in major hubs hit 6.1%, creating a mix of tight supply and rising costs as companies scramble to secure space.

This evolving market presents a window of opportunity. With average rents in the GTA sitting at $16.56 per square foot and a "Tenant's Market" emerging due to increased availability, businesses that move decisively can lock in favourable lease terms. Companies might consider renegotiating existing leases, exploring cost-effective areas like GTA East, where rents average $14.86 per square foot, or seeking high-quality sublease options in modern facilities. Acting now is crucial, as trade stability expected by late 2026 could reignite competition.

Successfully navigating these challenges requires expert guidance. Lennard Commercial - Industrial Real Estate Services provides the insights and strategies necessary to thrive in these conditions. Whether it's finding warehouses with 36'+ clear heights suited for automation or facilitating partnerships with third-party logistics providers to enhance flexibility, their expertise can make a significant difference. As Alan Dewar of GHY International aptly notes, "Warehouse demand isn't being driven by growth – it's being driven by uncertainty. Warehouses aren't just storage anymore; they're a front‐line tool for managing trade risk". With access to proprietary data and the market knowledge of professionals like Michael Law at Lennard Commercial, businesses can effectively balance immediate challenges with long-term growth.

FAQs

How much warehouse space should I add for safety stock?

It’s often advised to set aside an extra 10-20% of your warehouse space for safety stock. This buffer helps address supply chain disruptions and shifts in demand, which have been especially challenging in the Greater Toronto Area (GTA) given the increasing demand for warehouse space and persistent uncertainties in the market.

Should I lease, sublease, or use a 3PL in the GTA?

When deciding how to manage your warehousing needs in the competitive GTA market, it’s important to weigh your options carefully:

- Leasing: This option is perfect if you’re looking for long-term stability and control over your space. It’s a great fit for businesses with consistent storage and operational requirements.

- Subleasing: If your business needs more flexibility, subleasing can be a smart choice. It allows you to adapt to changing market conditions without committing to a long-term agreement.

- 3PL (Third-Party Logistics): Partnering with a 3PL provider lets you outsource warehousing and distribution tasks. This frees up your time and resources to focus on your core business operations.

Think about your company’s goals, budget, and growth strategy to determine which option aligns best with your needs.

Where can I find cheaper GTA warehouse rent right now?

When it comes to finding affordable warehouse rents in the GTA, secondary markets or areas with higher vacancy rates are your best bet. These locations generally experience less demand, which often translates to more competitive rental prices. While exact rates aren't specified, targeting regions with higher vacancies could lead to more budget-friendly opportunities.

Written by

Michael Law

Partner, Lennard Commercial · Industrial Real Estate Specialist