Commercial real estate Columbus Ohio: 2026 industrial guide

By Michael Law · Industrial Real Estate Broker, Lennard Commercial Realty

Commercial real estate Columbus Ohio: 2026 industrial guide

TL;DR:

- Columbus’s industrial market is highly active and supply-constrained, driven by demand from advanced manufacturing and data centers. Only 17 percent of its construction pipeline is available for lease, while vacancy rates are declining. Investors should act quickly, as available space is limited and lease negotiations favor landlords.

Commercial real estate in Columbus, Ohio is defined by its industrial sector, which has become one of the most supply-constrained and investor-active markets in the United States. Columbus sits at the geographic centre of the eastern U.S., giving logistics operators access to 60% of U.S. households within a single day’s drive. That structural advantage, combined with rising demand from advanced manufacturing and data centre tenants, makes Columbus commercial properties a priority target for investors and business owners in 2026. The Central Ohio Commercial Information Exchange (COCIE) and Moody’s Analytics now provide the market intelligence layer that serious investors need to act with confidence.

What are the current market dynamics shaping Columbus industrial real estate?

Columbus’s industrial market has tightened for three consecutive quarters, with net absorption running well above its three-year average. That sustained absorption signals genuine occupier demand, not a short-term spike. When absorption consistently outpaces new supply, vacancy rates fall and landlords gain pricing power.

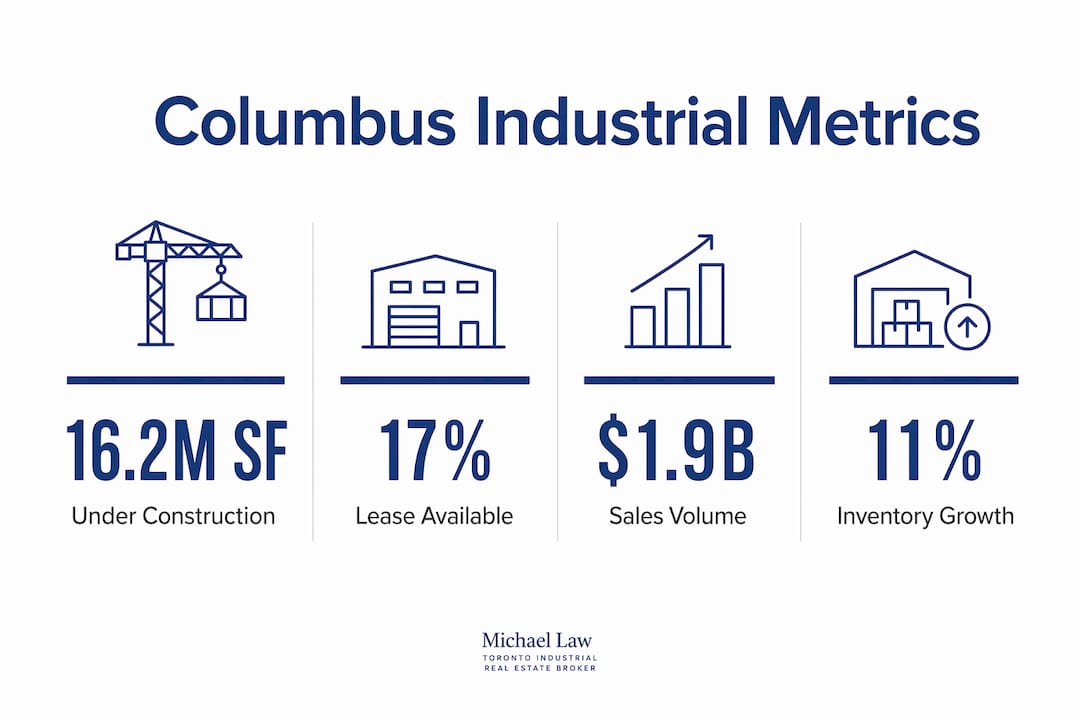

Sales volume in Columbus industrial markets totalled $1.9 billion over the past 12 months, exceeding the five-year average of $1.4 billion. Q1 2026 alone recorded a 45% year-over-year increase in transaction volume. Those figures confirm that institutional and private investors are actively deploying capital into Columbus commercial properties, not just watching from the sidelines.

Rent growth is following the same trajectory. Speculative development deliveries dropped to a six-year low in 2025, which removes the supply pressure that typically caps rent increases. Landlords are holding firm on asking rates, and tenants have less room to negotiate than they did two years ago.

The tenant mix reshaping Columbus’s industrial market includes:

- Advanced manufacturing operators requiring heavy power and specialised floor loads

- Aerospace and defence contractors such as Anduril, which demand secure, purpose-built facilities

- Hyperscale data centres from companies like Meta and Intel, absorbing large blocks of land and building area

- Logistics and e-commerce users competing for the remaining speculative space

Pro Tip: Track net absorption quarterly through COCIE’s partnership with Moody’s Analytics. When absorption exceeds new deliveries for two or more consecutive quarters, expect landlord leverage to increase and concessions to shrink.

The presence of data centre and advanced manufacturing tenants reshapes market dynamics by reducing the pool of available space for smaller logistics users. A warehouse operator looking for 50,000 square feet is now competing in a market where the largest blocks are pre-committed to hyperscale users. That compression pushes smaller tenants toward secondary submarkets and older product.

How does specialised development affect industrial property availability in Columbus?

Columbus currently has 16.2 million square feet under construction, but only 17% of that pipeline is available for lease. That figure is the most important number in the Columbus industrial market right now. A large construction pipeline creates the impression of abundant supply, but the reality is far more constrained.

The breakdown explains why. Approximately 28% of the pipeline is accounted for by build-to-suit facilities for major users including Intel, Meta, and Anduril. These facilities are purpose-built for specific occupiers and never enter the open market. The remaining construction is split between pre-leased speculative buildings and a small slice of truly available space.

| Pipeline category | Share of 16.2M SF | Available to general market |

|---|---|---|

| Build-to-suit (Intel, Meta, Anduril) | ~28% | No |

| Pre-leased speculative space | ~55% | No |

| Available for lease | ~17% | Yes |

For investors and business owners, this table reframes the opportunity. The headline construction number overstates supply. The real competition for space is concentrated in that 17% slice, which means landlords hold significant leverage over lease terms and pricing.

Smaller logistics and warehouse tenants face the sharpest consequences. When hyperscale users absorb the largest, newest buildings, secondary tenants are pushed into older product or must accept longer lead times on build-to-suit negotiations. A distribution operator that needs 100,000 square feet of modern dock-high space in Columbus will find fewer options than the headline vacancy rate suggests.

Pro Tip: When evaluating Columbus industrial properties, always separate raw vacancy from truly available speculative space. Ask the listing broker to confirm whether the space is immediately occupiable or tied to a pending build-to-suit commitment.

The speculative development slowdown is not a temporary condition. Higher construction costs, tighter construction lending, and longer entitlement timelines all discourage developers from breaking ground on spec buildings without a committed tenant. That structural constraint keeps the available pipeline thin and supports rent growth well into 2026.

What leasing and financing considerations matter for Columbus industrial investors?

Lease concessions, including tenant improvement allowances, are narrowing as vacancy declines. Two years ago, landlords routinely offered generous fit-out packages to attract tenants. That era is closing. Tenants who wait for a better deal may find that the deal they passed on was the best available. Understanding tenant improvement allowances and how they are structured is now a core negotiating skill, not a secondary consideration.

For tenants planning expansions or new leases, the timing of lease negotiations matters as much as the lease terms themselves. A business that begins its site search six months before lease expiry will face a compressed timeline and reduced negotiating room. The most effective tenants in Columbus’s current market start the process 12 to 18 months in advance.

Leasing steps that protect your position in a tight market:

- Audit your current space requirements against a 36-month operational forecast, not just current headcount.

- Identify three to five target submarkets in Columbus before engaging landlords, so you have genuine alternatives.

- Engage a tenant representative before approaching landlords directly. Landlords negotiate daily; most tenants negotiate once every five to ten years.

- Request a full concession schedule in writing, including free rent periods, tenant improvement allowances, and any landlord work commitments.

- Build a financing pre-approval into your timeline before signing a letter of intent on an owner-user acquisition.

Financing timelines add another layer of complexity for investors buying Columbus commercial properties. Bridge loans typically close in 4 to 8 weeks, while permanent institutional debt can require 45 to 90 days. A buyer who signs a purchase agreement without a clear financing path risks losing the deposit if the lender’s timeline exceeds the contract’s closing window.

Key financing considerations for Columbus industrial acquisitions:

- Bridge loans suit value-add acquisitions where the property needs stabilisation before permanent financing.

- SBA 504 loans work well for owner-users buying their own facility, offering lower down payments than conventional commercial mortgages.

- Permanent debt from life insurance companies or CMBS lenders suits stabilised, long-leased assets with creditworthy tenants.

- Construction financing requires a clear exit strategy, either a permanent loan takeout or a pre-committed tenant, before most lenders will engage.

Commercial lending timelines vary significantly by loan type, and that variance directly affects how you structure a purchase offer. A 30-day closing condition is realistic for a bridge loan but not for institutional permanent debt. Aligning your financing type with your contract timeline prevents costly renegotiations or failed closings.

How does Columbus’s location give industrial investors a competitive edge?

Columbus’s geographic position is the single most durable advantage in its industrial market. The city sits within a one-day drive of roughly 60% of U.S. households, making it a natural distribution hub for companies serving the eastern seaboard, the Midwest, and the South simultaneously. No amount of market softening elsewhere changes that physical reality.

Columbus’s industrial inventory expanded 11% over the past three years, compared to a national rate of 6.3%. That growth rate reflects genuine occupier demand pulling new supply into the market, not speculative overbuilding. Markets that grow faster than the national average on the back of real demand tend to sustain rent growth longer than markets driven by developer optimism.

| Market indicator | Columbus | U.S. national average |

|---|---|---|

| Industrial inventory growth (3 years) | 11% | 6.3% |

| Household reach within one-day drive | ~60% of U.S. | Varies by location |

| Q1 2026 sales volume vs. five-year average | $1.9B vs. $1.4B | N/A |

| Speculative delivery pace (2025) | Six-year low | Elevated in many markets |

The sectors driving Columbus’s industrial demand are not cyclical. Aerospace and defence contractors require proximity to Ohio’s manufacturing base and its skilled labour pool. Advanced manufacturing tenants, including semiconductor-adjacent suppliers drawn by Intel’s presence, need large power capacity and purpose-built infrastructure. Data centres from operators like Meta require stable power grids and fibre connectivity, both of which Columbus delivers.

Investors comparing Columbus to commercial real estate in Cleveland or commercial real estate in Dayton, Ohio will find that Columbus offers a larger and more liquid market. Cleveland’s industrial base is strong but more heavily weighted toward legacy manufacturing. Dayton’s market is smaller and more dependent on defence-sector cycles. Columbus combines scale, sector diversity, and logistics centrality in a way that neither Cleveland nor Dayton fully replicates.

Rent growth in Columbus has outpaced national rates as a direct result of the supply-demand imbalance described above. When you combine a constrained speculative pipeline with sustained absorption from high-quality tenants, rent growth follows as a mathematical outcome. Investors who acquired Columbus industrial assets in 2022 and 2023 are now benefiting from that dynamic.

Pro Tip: When comparing Columbus to other Ohio markets, weight logistics centrality and tenant quality above headline vacancy rates. A market with 4% vacancy driven by data centre and defence tenants is structurally stronger than a market with 3% vacancy driven by short-term logistics leases.

Key takeaways

Columbus industrial real estate is the strongest supply-constrained market in Ohio, with only 17% of its 16.2 million square foot pipeline available for lease and sales volume exceeding its five-year average by $500 million.

| Point | Details |

|---|---|

| Pipeline availability is narrow | Only 17% of 16.2M SF under construction is available; the rest is pre-committed or build-to-suit. |

| Absorption signals genuine demand | Net absorption has exceeded the three-year average for three consecutive quarters, confirming occupier-led growth. |

| Lease concessions are shrinking | Tenant improvement allowances are narrowing; tenants should begin lease planning 12–18 months before expiry. |

| Financing timing is critical | Bridge loans close in 4–8 weeks; permanent debt requires 45–90 days. Align loan type with contract timelines. |

| Location drives long-term value | Columbus reaches 60% of U.S. households within one day, making it a durable logistics and manufacturing hub. |

What I have learned from watching Columbus’s industrial market evolve

Columbus is one of those markets that rewards patience and punishes assumptions. I have watched investors walk away from Columbus industrial deals in 2022 because the cap rates looked thin relative to other Ohio markets. Those same investors are now watching Columbus sales volume hit $1.9 billion in a single year while their alternative markets stagnate.

The build-to-suit dynamic is the piece that most investors underestimate. When Intel and Meta commit to purpose-built facilities in a market, they do not just occupy space. They reshape the entire tenant ecosystem around them. Suppliers, contractors, and logistics operators follow those anchor tenants, and they all need space. The 17% availability figure in Columbus’s pipeline is not a sign of a healthy, balanced market. It is a warning that competition for quality space will intensify, not ease.

My honest view on leasing in Columbus right now: tenants who approach the market the way they did in 2020 or 2021, expecting landlords to compete for their business, will be disappointed. The industrial real estate trends in 2026 point clearly toward landlord-favourable conditions in supply-constrained markets. Columbus is at the front of that trend. Tenants need to come to the table prepared, with financing arranged, requirements clearly defined, and a realistic view of what concessions are still available.

For investors, the financing coordination point is not optional. I have seen acquisitions fall apart at the last stage because the buyer assumed a 30-day close was achievable on permanent institutional debt. It is not. Build your timeline around the loan type, not the other way around.

Columbus is not a market to approach casually. The data is clear, the demand drivers are durable, and the window for favourable entry conditions is narrowing. Act on information, not on hope.

— Michael

Industrial real estate advisory for Columbus and beyond

Mlawrealestate brings institutional-grade market intelligence and transaction expertise to investors and business owners evaluating industrial properties across North America’s most active markets.

Whether you are looking to invest in Columbus real estate, secure warehouse space, or evaluate an owner-user acquisition, the Mlawrealestate team provides the data and negotiating experience to position you ahead of the market. Michael Law’s affiliation with Lennard Commercial Realty adds depth to every transaction, combining local market knowledge with institutional-grade advisory. Browse available industrial property listings to see current opportunities across industrial markets, and connect with the team to discuss your specific requirements before the available pipeline tightens further.

FAQ

What is commercial real estate in Columbus, Ohio?

Commercial real estate in Columbus, Ohio refers to income-producing properties used for business purposes, including industrial warehouses, logistics facilities, manufacturing plants, office space, and retail real estate. The industrial sector is currently the most active and supply-constrained segment of the Columbus market.

Why is Columbus a strong market for industrial investment?

Columbus reaches approximately 60% of U.S. households within a one-day drive, making it a premier logistics hub. Industrial inventory grew 11% over three years, outpacing the national rate of 6.3%, and sales volume hit $1.9 billion in the past 12 months.

How much of Columbus’s industrial construction pipeline is available to lease?

Only 17% of the 16.2 million square feet currently under construction in Columbus is available for lease. The remainder is pre-committed through build-to-suit agreements for major users including Intel, Meta, and Anduril.

How long does commercial real estate financing take in Columbus?

Bridge loans typically close in 4 to 8 weeks. Permanent institutional debt requires 45 to 90 days. Investors should align their loan type with their purchase contract timeline to avoid closing delays.

How does Columbus compare to commercial real estate in Cleveland or Dayton?

Columbus offers a larger, more liquid industrial market with greater sector diversity than Cleveland or Dayton. Cleveland skews toward legacy manufacturing and Dayton is more defence-dependent, while Columbus combines logistics centrality, advanced manufacturing, and data centre demand in a single market.

Recommended

About Michael Law

Managing Partner and Industrial Real Estate Broker at Lennard Commercial Realty. Representing tenants and landlords across Toronto and the GTA for 15+ years. Michael specializes in GTA industrial real estate — connect with Toronto's leading industrial broker at mlawrealestate.com/industrial-broker-toronto.